Cash Flow Is Cash, But Better

To hold cash, or not to hold cash. That is the question.

To hold cash, or not to hold cash. That is the question.

Over the years, I’ve witnessed consternation on the part of fellow dividend growth investors either directly through emails I’ve received or via passing comments in regards to whether or not and/or how much cash should be held on the sidelines, awaiting opportunities to deploy it.

Should we hold cash? How much cash should we hold? Warren Buffett holds billions of dollars in cash at any given time, so we should probably hold cash as well, right?

I’m going to discuss this a little bit today.

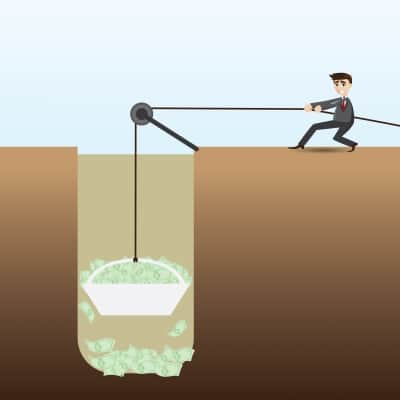

Start Digging

First off, I want you to realize that if your whole goal in life is to dig a giant hole, you’d be better off constantly and consistently digging, rather than sitting around collecting shovels.

And there are parallels to those of us whose major investing goal is to build enough passive dividend income so that expenses are covered, thus freeing us from wage slavery to pursue our passions or otherwise spend our time in a way that’s most becoming to us.

What I mean by that is that every dollar not invested in cash flow-producing assets is a dollar that’s not freeing you by working for you. If working at a job you don’t particularly enjoy is a version of prison cell, then every dividend dollar that hits your account can be likened to an imaginary digger, slowly chipping away at the rock and dirt that sits between your cell and the outside world, beyond the prison walls.

I’ve Never Held Much Cash

I’m perhaps biased. I’ve been incredibly anxious to invest cash almost as soon as it has hit my hands ever since I started actively investing back in early 2010. Holding unproductive cash for any lengthy period of time just didn’t make sense to me. After all, stocks offer an average annual return of around 7% over the long haul, after factoring inflation. That’s your real return.

Cash, meanwhile, loses value. Inflation ravages cash over time – so much so that $1.00 of purchasing power in 1994 now requires $1.61 for the same purchasing power. So something that cost $1.00 20 years ago would now cost $1.61, all else being equal.

Now that’s over 20 years. Cash doesn’t lose value to inflation so quickly to where holding cash for a month or two will hurt you, right?

Well, that’s correct. But we’re not talking about holding cash for a month. If we were, you’d be regularly investing like me. We’re talking about holding a substantial portion of cash on the side for however long it takes for a notable market opportunity to present itself. Perhaps where stocks become so cheap that you can’t ignore them.

In that case, I’ve got bad news for you. The broader stock market – the S&P 500 index – has increased by 94.7% over the last five years. And they’ve almost moved in a straight line up, about as straight as stocks can go.

Maybe that means stocks have to correct from here. But maybe not. What I can tell you, though, is that someone who’s been waiting for a big stock market correction over the last five years to deploy capital has been doing a lot of waiting.

I’ve been hearing about how crazy I am to not hold a lot of cash for over two years now. I can’t tell you how many emails I’ve received or articles I’ve read over the last 24 months or so that indicated that the stock market was going to crash. The charts say so, or interest rates are going to rise, or the Fiscal Cliff is going to cause stocks to go over a cliff, or the solar eclipse is a different shade of black.

But you know what I’ve been doing over the last two years?

I’ve been busy ignoring the noise and consistently investing in high-quality stocks that pay and grow dividends. And my portfolio has grown from $81,000 to almost $178,000.

So much for cash.

Cash Flow Is Cash, But Better

See, what I’ve realized that there is something much, much better than cash: cash flow.

Cash flow is cash, but it’s way, way better. And I’ll tell you why.

So I’ve already discussed how much my portfolio has grown, but that’s really of minor importance. What is actually quite important is the cash flow via growing dividend income that the portfolio now generates.

My portfolio of 51 dividend growth stocks is now generating almost $6,000 in annual dividend income for me.

Did you catch that?

By not holding on to cash I’ve actually built a machine that generates cash every single month, on the order of approximately $500 per month (averaged out).

So I don’t need to hold cash in order to “take advantage of the dips”. My portfolio produces the cash flow – real cash money, folks – necessary to buy stocks routinely and consistently, without the necessity to hold on to a big pile of rotting and shrinking cash. My cash pile is being replenished for me every time I spend it. I invest $500. And then a month later I have another $500. Even better, this cash flow is growing due to the power of reinvestment and regular investment of my other cash flow that comes from work on my part.

So let’s say I could give you a choice of two buckets: one that holds $6,000 in cash that once spent is gone forever, or one that magically refills itself with $6,000 every 12 months and is likely to increase that amount over and above the rate of inflation annually. Which would you choose?

What I realized early on is that, as an investment, cash by itself offers me little utility, other than to work for me. If it’s not working for me it’s not providing any value at all. And I turned that realization into an incredible work ethic for my cash, where I’m basically an intolerable boss who requires my cash to work 24 hours per day, 365 days per week. I offer no holiday pay, no sick time off, and no vacations. I’m miserable. And every single time I have a new hire, I put that new hire to work right away. What’s even better is that these workers recruit new workers for me, compounding my work force!

Compounding And Opportunity Cost

This is because cash compounds itself when it works for me. Keeping $1,000 on the side, waiting for “an opportunity” that may or may not come seems silly to me when I already have “an opportunity” right in front of me to buy 25 shares of Kinder Morgan Inc. (KMI). Those shares will likely appreciate over a long period of time, regardless of the stock market’s ups and downs in the interim, due to the high-quality, cash flow-producing assets that the underlying company owns in the energy space. Furthermore, those 25 shares pay me $44.00 per year in the form of a dividend. And I can reinvest that $44.00 back into KMI shares, buying more than one share per year, which will also pay me a dividend. So not only am I growing my cash flow via the reinvestment of that dividend income, but KMI continues to increase its dividend annually – the company is projecting 10% annual dividend growth during the 2015 – 2020 period. Thus, I’m reinvesting cash flow into an asset that just so happens to also be growing the cash flow it’s paying.

Growing cash flow by reinvestment into cash flow-producing assets as well as growth via the asset itself paying out more cash flow. It’s enough to make you question what exactly an “opportunity” really is and why you’re busy waiting around.

Holding a lot of cash on the side may seem smart due to opportunity costs. The thought is that if stocks do indeed decline by a marked amount then there’s an opportunity cost of being fully invested or close to it because you won’t have capital to strike.

However, the flip side is the opportunity cost I just laid out in front of you. I could have held $10,000 in cash over the last two or three years, after stocks started noticeably appreciating. But there is just as much of an opportunity cost there as well. And that opportunity cost is the dividend income I’m now receiving and the value of the portfolio as it stands today. The opportunity cost is in the cash flow I’m now producing which I wouldn’t have otherwise been enjoying this entire time had I kept more cash aside.

Furthermore, by investing your cash into high-quality stocks that are attractively valued on a regular and consistent basis, your cash flow via the growing dividend income these stocks pay will grow over time. Thus, your “opportunity cost” naturally reduces itself over time. When you’re producing $1,000 or $2,000 per month in dividend income you don’t really have to worry about opportunity costs anymore. And that’s because your proverbial magic bucket is refilling itself so often and so aggressively with cash flow that you never lose a chance to strike when the iron is hot.

When To Strike?

But if you are the type of person who sleeps better at night with $5,000 or $10,000 in freely available cash that can be invested at any time, then more power to you. No investment return is worth losing sleep over.

However, I do sometimes question the strategy of holding on to a lot of cash in regards to timing and deployment. I’d like to think I’m rational and intelligent, and so I can understand the value in having some cash on the side if/when calamity strikes and the market takes a serious drop. However, when exactly do you deploy cash if/when this happens? If the S&P 500 falls by 5%, do you strike then? What if it falls by another 5% the next week? Did you strike too early? Do you instead wait for a 10% drop – a full correction? What if that’s just the start of something more sinister?

The problem with holding more cash than what is set aside for regular investing, in my view, is that there is no perfect time to deploy it. And that’s because we can’t time the market. You have no idea when it’s just the right time to finally release that cash and get it out there working for you, because you don’t know what’s next. You start paying attention to the noise and think the 8% drop over the course of a week is the start of global turmoil, only to watch it bounce back shortly thereafter. Now what?

It’s like we recently witnessed just this past month. The Dow Jones Industrial Average fell by 1,000 points from October 8th to October 15th. 1,000 points. Do you let the cash go after 500 points? Or 1,000? Is the 1,000 the harbinger of better opportunities? Well, you had to act fast, because the DJIA bounced back just as fast – up by 1,000 points by October 24th.

You can’t time the market. But you know what is fairly easy to time? The Coca-Cola Company’s (KO) dividend payout schedule. With 52 consecutive years of dividend raises and quarterly dividend history dating back to 1920, I’m fairly confident that next dividend and the dividend after it are going to hit my brokerage account. And this exercise can be repeated for the other 52 companies I’m invested in.

So the market can’t be timed. But my cash flow can.

Cash Flow Your Life

Although I don’t keep a lot of capital on the side and I’m typically pretty fully invested, that doesn’t mean I can’t invest relatively aggressively in stocks when equities do indeed become cheaper. I’m not missing out on any new opportunities, even while I take advantage of the opportunity of cash flow my portfolio generates.

For instance, this past month was volatile, as I touched on above.

And what did I do?

I deployed more than $4,400 over the past month.

I was able to do that because I cash flow my life. I live below my means and create a sizable gap between my income and expenses, thus leading to a constant surplus of capital with which I can invest. And of course there’s that dividend income I touched on above. So the difference between my income and expenses has been somewhere around $2,000 lately. Add in the $500/month average dividend income and that’s $2,500. I also maintain an emergency fund of somewhere around $5,000 that I can always tap in case a real emergency actually befalls me, or in case cheap stocks start calling my name. And so I tapped into that fund a bit this past month, which means I’ll have to rebuild it slowly now that the market, and many stocks within the market, have rebounded a bit.

I get that someone who holds thousands of dollars in liquid cash on the side probably sleeps well at night and has all kinds of warm and fuzzy feelings. But don’t think that if you don’t hold a bunch of cash on the side that you can’t take advantage of volatility when it presents itself. You simply have to cash flow your life and create a regular surplus of capital so that you’re investing in the ebbs and flows of the market- dollar cost averaging your way in over a long period of time. This creates a whole new source of cash flow all by itself, thus increasing your surplus and your ability to take advantage of opportunities.

I personally invest just about every single month, and have done so for more than four years straight. And I typically invest multiple times per month, thus catching opportunities every couple of weeks or so. You just can’t be much more opportune than that, in my opinion. And you can invest just like this if you cash flow your life appropriately.

But What About Warren Buffett?

You’d be hard pressed to find a bigger fan of Warren Buffett than me. I’m currently re-reading his biography. No easy task when the book is 900 pages. Furthermore, I’m planning on visiting the Berkshire Hathaway Inc. (BRK.B) annual shareholders’ meeting in 2015 as part of my honeymoon. Yeah, I’m a fan.

And so I never fail to notice when people cite Warren Buffett on the topic of holding cash in case there’s a major stock market correction.

For instance, Buffett, via Berkshire Hathaway, currently has more than $50 billion in cash and equivalents at his disposal. He calls this kind of capital his elephant gun, and rightly so.

And there was this quote in the 2008 shareholders’ letter:

I have pledged – to you, the rating agencies and myself – to always run Berkshire with more than ample cash. We never want to count on the kindness of strangers in order to meet tomorrow’s obligations. When forced to choose, I will not trade even a night’s sleep for the chance of extra profits.

I admire that conservative nature. And I also applaud it and agree with it.

However, it’s important to note that Berkshire Hathaway is a $345 billion company. Let me repeat that. It is a $345 billion company. Buffett requires a fair measure of cash on hand due to the nature and size of the company, which includes substantial insurance operations. But I don’t run a $345 billion company. And I’m quite sure you don’t either. The comparisons to Warren Buffett and Berkshire Hathaway are therefore completely misplaced and just not applicable.

Sure, they don’t need anywhere near $50 billion to cover short-term obligations, and so some investors are speculating that he can’t find any elephants – stocks/companies aren’t cheap, so goes the thought. But I think those same investors have glossed over the fact that he’s been routinely taking down elephants over the years, even quite recently. These elephants then continue to grow his cash flow to the point where now it’s becoming difficult for him to actually spend/invest it in an appropriate way to meaningfully move Berkshire’s needle. But I don’t have that kind of needle to move. It’s quite easy to move my needle.

So take 2008, the year I cited above for that quote. Berkshire ended that year with less than $26 billion in cash. Fast forward to 2013, Berkshire spent $18 billion on two major acquisitions: NV Energy Inc. and a portion of H.J. Heinz Company. Now Berkshire has over $50 billion. Do you see how that works? He continues to take down elephants, but those elephants happen to produce prodigious cash flow, thus increasing the amount of ammo in his elephant gun for his next hunting trip. His elephant gun is actually reloading faster than he can hunt, exactly because he’s deployed capital with some regularity over the last 50 years. Buffett is cash flowing his life (and his company), though on a much larger scale than you or I can imagine.

However, while Buffett currently has a $50 billion cash pile that builds up, I also want to point out that Buffett wasn’t always so eager to hold on to cash. Buffett wasn’t always running at $345 billion company that took major acquisitions to meaningfully impact the bottom line. What about a young Warren Buffett, a Buffett that would be more aptly comparable to a situation that we might find ourselves in? Well, I don’t know if we can ever aptly compare ourselves to the greatest investor of all time, but a young Buffett is at least in the same universe.

Consider this quote, from page 283 of Buffett’s biography, “The Snowball: Warren Buffett and the Business of Life”:

In January 1966, another $6.8 million had rolled in from his partners; Buffett found himself with a $44 million partnership and too few cigar butts to light with his cash. Thus, for the first time, had had set aside some money and left it unused – an extraordinary decision. Ever since the day he left Columbia Business School, his problem had always been getting his hands on enough money to pump into a seemingly endless supply of investment ideas.

So Buffett’s problem as a young investor anxious to increase his wealth as quickly as possible was to find enough cash to invest. Buffett didn’t slow down putting capital to work until his partnerships had eclipsed $40 million. I assume you don’t have a first world problem that aggressive. I know I certainly do not. Which is why I continue to invest capital almost as fast as it hits my tiny pocket.

Conclusion

I recommend that unless you’re already sitting on a portfolio worth well over $100,000 that’s spitting out at least $3,500 in annual dividend income, you should continue to dollar cost average your way into the stock market month in and month out, regardless of the media noise, the predictions, or your desire to sit on cash. In fact, I would recommend continuing this strategy straight through to financial independence, but I can relax my attitude on this just a bit if you’ve already developed a cash flow bucket that refills itself with at least $300 per month with which you can dump on new opportunities. However, I personally wouldn’t feel comfortable with more than 2% of my portfolio sitting in cash for any time frame longer than a couple of months during the asset accumulation phase for the reasons I’ve laid out. That is, not until I’m very close to financial independence or already financially independent and capital preservation is even more critical.

That being said, if you are close to financial independence or already financially independent then you’re likely already cash flowing your life with passive income, and thus any cash flow surplus that represents the spread between income and expenses can be used to build a substantial enough cash cushion so that you feel completely comfortable. I’ve already discussed in the past that I would want to increase my emergency fund slowly and surely past the point of financial independence, so as to constantly increase my margin of safety due largely to the fact that unforeseen medical problems become more likely as you age.

However, if you’re a new investor with a portfolio worth $20,000 or $50,000 I truly believe you shouldn’t even be considering the idea of sitting on cash. You need to get those dollars digging for you as soon as possible. This isn’t the time to collect shovels. This is the time to be actively digging your way out to freedom. You may be thinking that there’s an opportunity cost in investing your capital relatively quickly, but your true opportunity cost is in not already having a significant source of recurring cash flow with which you can regularly tap to increase your wealth at an even faster pace.

I find the comparisons to Buffett fun to entertain, but they’re just not really applicable to a retail investor. We don’t run $350 billion companies that require major acquisitions to move the needle. The aforementioned purchase of 40 shares of KMI would move my needle right away, which is why I deploy capital so frequently and enthusiastically. Buffett may sport an elephant gun, but I proudly shoot my BB gun with regularity. And it regularly reloads itself!

As a final note, I’m not recommending to forgo an emergency fund. That should be separate. This is specifically discussing the cash portion of your investment portfolio. Like Buffett’s desire to not rely on the kindness of strangers, I also do not want to be in a position where I’m forced to borrow money at disadvantageous rates in the case of an emergency. However, I also keep in mind that a six-figure portfolio that has been built by putting capital to work regularly, and produces a source of cash flow that could be used in an emergency is really the ultimate form of an emergency fund anyhow.

Full Disclosure: Long KMI and KO.

What do you think? Do you typically sit on a sizable portion of cash, or are you more interested in building cash flow? Is cash flow better than cash?

Thanks for reading.

Photo Credit: iosphere/FreeDigitalPhotos.net

You will like the Berkshire annual meeting for sure. It was on my bucket list, and honestly, while Warren was great, Charlie was fantastic; it was like a counseling session, financial planning lecture, finance class, life lessons, comedy show and shopping at a discount mall all in one location.

Dividend Mantra,

My cash position is large right now. I am actively researching and looking to put that money to work in purchasing stocks that will pay me dividends. I sometimes sell a put option in a stock that I am trying to buy. When a sell the put option I receive payment in the form of a premium also. Other times I buy via limit orders such as I did with BBD.B stock.

Have you heard of the concept called “placeholder”? A while back, Mohnish Pabrai used Berkshire Hathaway as a placeholder for cash. So rather than hold cash, he would invest in securities with very to no downsize risk such as SPACs, Berkshire Hathaway, Fairfax Financial, etc. He eventually stopped using that concept because he had a high hurdle rate to obtain for his investors. But I think that concept might work well for say an emergency fund.

DM.. Excellent article. Well written. Buffett keeps that cash for certain reasons and at this point he needs a lot of that cash to make the outsized buyouts of large companies. He’s in a different arena than me, you, or any FI pursuer.

For my circumstances, I tend to keep a lot of cash. I’ve got a few rental homes. I’ve got large medical bills for a chronic illness. I tend to keep 6-9 months worth of living, rental properties, and medical bills worth in cash. It is a substantial amount due to the rental homes & medical bills, but I sleep so much better knowing its there.

I have been building up a large portfolio over 2014 and have a limited supply of cash that continues to increase due to my high savings rate of my day job.

Since I work in Asia I usually move out large chunks of cash periodically back to the USA for more investing but like to have a buffer of several months to a few years of living expenses. Fortunately I can replenish this in just a few months of working so all is well.

-Mike

I put it in to work as soon as i get paid. The sooner I have the money working for me the sooner I get growing dividends. Great write up.

DM,

Great post and great timing for it – given the volatility over the last month in October. I am also a guy who doesn’t like to hold cash and actually, sad to say it – complains when i have too much cash sitting there… earning me absolutely nothing and not working hard for me – as you also have put it.

Buying dividend stocks with cash is clockwork – buy appreciating assets that produce you cash flow that can be reinvested to grab more assets (shares) that continues to produce cash… and also there are increases to how much cash goes back as well – so it’s a double uptick to the “cash flow” in forms of dividends. It’s amazing. Cash can sit there in an account earning 0.00% to 0.75% and I can guarantee – it probably won’t get you anywhere.

October was the same month for me – I unloaded quite a bit of capital during that downturn spell and was pumped about it. I don’t and can’t predict dips, instead – I regularly invest. However – similar to you, I always have $5-$8K in cash reserves that I “tap” into when volatility hits and it definitely hit in October.

I agree as well with having enough cash to sleep at night in case of emergencies – however, a good evaluation of how much is actually needed to help you sleep at night can paint a much better picture than saying “$20K” or “$10K”. What if your expenses were only $500 a month? Do you really need 40 months of living expenses in cash reserves? You probably would be fine with $2,500 in cash reserves and not $20,000.

Great article and as an investor – a great read. Summary: Invest, invest often and keep enough cash to make sure you are confident in sleeping and don’t be afraid to tap into it during volatile stock market swings. Long comment DM haha, so I apologize, but definitely like the goal and article. Hope you had a nice weekend, talk soon.

-Lanny

We are definitely guilty of holding too much cash…hopefully, in a year of so I will be able to say that is no longer our family. For a few years now, being a single income household and a weak job market, we were forced to sit on more cash than we would have liked.

If you follow our journey, we’ve been diligently spending our capital this year. My job and the job market is in a much better place now. And as our confidence rose, we slowly have found the courage to move away from cash and spread our money throughout various income producing investments. I must admit that our passive income has grown significantly in 2014 and could only imagine what it would have been like had we moved away from cash sooner.

AFFJ

I was looking all over your site this weekend for this type of article. I searched for every cash flow/ emergency fund article, but none were as detailed about cash flow and opportunity cost as this. It’s like you read my mind and wrote the article I was looking for. Also the article itself is an awesome reference to my name and digging money.

I definitely agree that starting out capital needs to be allocated to investments that will start producing cash flow. Passive cash flow is king as it can then be diverted to whatever investment is the most opportune at that time. I keep thinking about the analogy of how your portfolio is a “Machine” and the fuel for it is cash. The machine runs on fuel and the machine rewards you by creating more fuel. If you provide the machine enough fuel it will basically become self sufficient. Right now it appears your current machine takes in $2,000 worth of fuel each month, originally all that fuel was provided by active income, but now $500 is subsidized each month by the machine so it only needs $1,500 from external sources to get the full $2,000. Once the machine becomes self sufficient (providing $2,000 worth of monthly income) it will be providing more fuel on its own than you could have originally supplied it. That will be an interesting moment there because you will have effectively created a clone of your original self. This clone will soon create another machine and another and another and so on.

You will essentially have an army of money making machines and the cycle can only be averted if you decide to liquidate the machines and take more fuel from the machines than they are providing. I’ve seen where you have stated that once you reach FI that you are done. I don’t recall what your exact number is, but I know you stated that it is essentially equal to your total living expenses. If that is the case you will only need to have created one clone of yourself since you are effectively already saving 50% each month, the same amount as original fuel for the machine. I hope your plan is to live off an amount that is under the amount the machine is producing. Otherwise you will start to breakdown the machine and in my opinion that is an unnecessary risky move. I personally would feel more comfortable knowing that I have an army of unbreakable machines creating clones of myself so that I never have to depend upon “active” income ever again. Also these clones will create a continuous raise in living expenses all on their own and at an exponential rate.

Great article

Everybody has different needs and its crucial that we recognize them just like how Alex recognized his. Having some cash on the sideline makes more sense , if I am on Alex’s shoes I would probably hold the same amount of emergency fund. But right now I have 2 months worth of emergency fund based on my needs just in case something happened (knock on wood). For me there is no wrong or right answer about how much or where the emergency fund is, it all depends on the person’s need. Younger healthier people have more leverage as they dont need as much emergency fund compared to older people or people that have health condition. Regarding timing the market, I dont believe in timing the market either as nobody can see the future. What I do is I regularly invest to avoid timing the market and when there is an opportunity just like the October drop, I use a portion of my emergency fund to take advantage of it then replenish my emergency fund slowly. Great article as usual DM!

FFF

Keith,

Sounds like a good time right there. Glad you got to check off a bucket list item and make it over there. I’m excited to go! 🙂

Thanks for dropping by and sharing.

Cheers!

IP,

Well, everyone’s definition of “opportunity” is probably a bit different. I usually have a hard time not finding attractively valued high-quality stocks, but I suppose that’s a gift and a curse of sorts. You may see opportunities a different way, but fulfilling your goals and staying on track is really what matters most.

Best regards.

Henry,

I’ve not heard of holding cash like that. And I don’t think that’s the best way to do it. Even the venerable Berkshire stock took a pretty big tumble during the financial crisis. I’d rather hold cash in an extremely safe and liquid place. A MM account would be a good example. Or a savings account. Short-term CDs are also a good place, in my view. This is for emergency funds, which is outside the scope of this article. I keep cash for investment purposes inside my brokerage account, which can be invested at any given time fairly immediately.

Cheers!

Alex P,

Thanks! 🙂

I hear you there. We all have different circumstances, which means our cash needs are also different. If I owned a home, for instance, I’d feel less comfortable with the amount of cash I keep on hand. Same goes if I had a large family to provide for. So circumstances chance how much cash you need for an emergency fund. Though, this article was specifically discussing cash for investment purposes, which also varies from investor to investor. As I stated at the end of the article, I’m not advising to change your emergency fund or invest that cash. Rather, if you hold $5k or $10k in free cash outside that emergency fund and you’re constantly waiting for the “perfect time” to invest it, the opportunity cost could be larger than you think.

Best wishes!

Mike,

You’re in a great spot there! It takes me a little longer to replenish a large supply of cash. I guess that’s why I’m so eager to get the cash flow pumping. I need that bucket filled! 🙂

Thanks for dropping by.

Best regards.

FFdividend,

I’m with you all the way. The sooner I get my cash working for me, the sooner I don’t have to work for my cash. 🙂

Take care!

Lanny,

Right. Absolutely. Circumstances are different for all of us, which affects what kind of liquid assets we require on hand. Although, I think it’s universal that more cash flow is a good thing. 🙂

Appreciate the support very much. And I’m in the same spot as you – never enough cash to invest. I couldn’t imagine sitting on $10k or so of cash in my brokerage account, especially when I know that’s 10,000 little diggers that could be slowly digging.

Thanks for dropping by!

Best wishes.

AFFJ,

That’s great that your confidence has grown, which also feeds into your ability to deploy capital and get the passive income flowing. It’s tough to make that jump when you have a lot of cash on hand making you “feel good”. But knowing the value of cash is slowly declining, I lack that warm and fuzzy feeling. Rising cash flow, however, does give me that feeling. So that just kind of feeds into itself, and builds those feelings over time.

Keep it up! 🙂

Cheers.

TayDiggsMoney,

Exactly. The machine is like a 3D printer that’s busy printing another 3D printer. So on and so forth. 🙂

I definitely plan to start living off of the dividend income once it exceeds my expenses. But I think the margin of safety will build itself, as I’m confident the dividend income growth will outpace my spending growth. That will create a gap between dividend income and spending that widens over time, likely creating a situation over time where the income is far more than I can spend. I imagine philanthropy will enter the picture at some point there, which would be a wonderful situation to be in. I guess we’ll see.

I’m glad this article was exactly what you were looking for. I try to always create new content here and I aim to repeat myself very little. I hadn’t really covered this topic quite like this before, so I felt it was about time I changed that. I’m very happy you found some value in it.

Thanks for the support!

Best wishes.

FFF,

Thanks for stopping by!

I think there might be some confusion here, though. I mentioned toward the end of the article that this piece isn’t speaking to one’s emergency fund. One should always keep enough cash for emergencies, and everyone’s circumstances are different.

This article is instead directed toward the amount of cash you may or may not keep on hand for investment purposes. Some investors out there have a fully-funded emergency fund and then keep thousands of dollars aside on top of that to deploy if/when particularly cheap stocks become available. That’s really what I was writing about here. I think one should think carefully about keeping a lot of cash on the sidelines for investment purposes, as there’s an opportunity cost in doing so.

For instance, I keep cash aside for emergencies. But I could very easily stop buying stocks for 3-5 months and build up $10k or more in cash. That’s the kind of behavior that I’m recommending to avoid for the reasons laid out. 🙂

Thanks for the support!

Best wishes.

The moment cash hits my account, it gets invested within a few days, at most. I don’t bother trying to time the market – I tried that in the past and found that I was absolutely horrible at it. Plus, I dislike seeing idle dollars in my brokerage account. I’m a slave driver! 🙂

On a side note, I am recovering from the flu but was lucky to have picked up The Snowball from my local library before I fell ill. Spent my bedridden weekend alternating between sleeping and reading. I’m only 200 pages in, but I really like it so far! I definitely didn’t expect Warren Buffett’s childhood to be so…colorful. Haha.

Hope you had a good weekend! I hear Interstellar is an amazing movie, though I haven’t had a chance to see it yet.

Did you write this article for me? 🙂 I know in the past we have often commented on the merits of deploying all cash or keeping a stash on the side for those inevitable dips that always seem to come our way. And, like you have commented on several of my articles, it’s “Hard to paint anything in investing with a broad brush.” So the question that comes up is, “how much cash do I keep on the side?” And of course, the answer is, “it depends.” It depends on the individual investor, the portfolio at hand, the risk tolerance of the investor, market and stock valuations, etc. In other words some amount of cash should always be on the sidelines. Whether it’s 1% of your portfolio or 50% or somewhere in between or even greater, it all comes down to the individual investor. You should put up a poll in this post and ask how much cash each of us hold. Interesting to see the results.

DivHut,

Well, this is one of those age-old issues. It’s definitely impossible to come up with any standard number that applies to everyone, though I would caution those with portfolios worth less than $100k against holding any substantial capital for any long period of time for the reasons laid out. It just doesn’t make sense, in my view, to hold a lot of cash on the sidelines at that point. The portfolio isn’t big enough to really get things rolling for you. Once you have that bucket regularly refilling itself you could maybe make a case for being a bit more strategic/selective with cash deployment, but I would still argue that it’s better just to constantly deploy capital. Keeping a bunch of cash on the side purposefully in hopes of cheaper stocks at some future unknown date is a form of market timing, which very likely just isn’t going to work out in your favor.

Thanks for dropping by!

Best regards.

Fantastic article my man! Exactly what I needed to finally make the decision to start portioning my “saved for a better opportunity” money into the market!

I still think I will keep a smaller amount for at better opportunity but I sure as hell dont need to have 12000 dollars lying around doing nothing for me.

So together with my monthly savings I will now portion out those savings on x amount of months so they can start doing the job for me!

It’s 07.54 here in Sweden now so I need to get my ass to work but thanks again for the eye-opening article and have a great day!

Martin

Absolutely correct, Jason. No one can time the market, so it is completely pointless to hold cash until the best buying opportunity knocks on the door. It will not knock on the door! I’m not buying into the stock market, but I’m buying into a market of stocks. I know that at each moment there are good quality stocks available that are below or at fair valuation. And when I find one I buy it which the cash that I have available for investing, regardless of what the broader market situation is. And as of that moment another little free cash flow pump starts working :-). Consistency is the name of the game.

Take care.

I just to have a bigger emergency fund that I really needed because of my job situation. Now I feel more secure of my job and was looking for investment opportunities. Then came the dip and I put my lazymoney to work! I bought JNJ, UL and Finnish Company called Nokia Tyres. Especially with these interest rates I don’t want to hold on to too much cash.

Great article again, thank you for it!

-Ville

Hi DM,

I’m totally with you on this one – I’m always anxiously awaiting my next lump-sum payment, so I can put it straight to work in one of the stocks on my watchlist. I do like to wait until I have at least $2-$3k to invest at once, which occasionally takes some time, but I have never had a shortage of investment ideas (not that they’re all necessarily great ones in hindsight!)

Great article, and really liked the digging analogy – always great to bring a slightly different perspective to these classic investment issues!

Cheers,

Jason

Hi DM

Great article there!!!

Like you, I dont hold much cash for an investment opportunity as that means you are probably going to time the market which begs the question when do you actually strike. I still have an active income every month so that will work should the market presents an opportunity to invest. The only cash you should be holding on is probably emergency funds related. Other than that cash is only decreasing your roe over time.

Since we are at this topic, I just wonder whether you have the same preference for companies that doesnt hold much cash in their balance sheet. What is applicable to you in real life may be applicable to the companies you are vested in as well. I just wonder if there are any correlation to that.

B

http://Www.foreverfinancialfreedom.blogspot.com

I generally don’t hold much cash on hand for very long either. I’m of the opinion that the money spent paying off loans, mortgages or investing is a better use of the funds. Put those guys to work!

I think that if you’re debt free and living below your means, you can cash flow most emergencies in a given month. On the other hand, a HELOC (if you’re a homeowner) or a personal line of credit is a much better option. If you do have a small emergency, you can pay it back in a relatively short amount of time. I’m one of those that feels a credit card makes for a sufficient emergency fund. Why keep those diggers on the sidelines when you can use other people’s money to stand by for the “who knows when?”

I’m a little less than two months away from knocking out the 2nd of three rental property mortgage payoffs, right on schedule. Down to a balance of $73,833 from $177,650. I’ve put every available cent to work paying off those mortgages and it’s really cool to see all the interest monies saved.

Great article DM!

The thought of holding cash has really crossed my mind a lot the last year.

Thinking of it as an opportunity cost (when not invested) certainly is a great way of looking at it.

“However, it’s important to note that Berkshire Hathaway is a $345 billion company. Let me repeat that. It is a $345 billion company. Buffett requires a fair measure of cash on hand due to the nature and size of the company, which includes substantial insurance operations.”

Exactly. Talking about Buffett can be fun sometimes but it’s totally an apples-to-oranges comparison for all of the nonbillionaires out there. Looking at his habits 50 years ago is much more insightful, as you pointed out.

DM, I recently opened an account at Optionshouse with 10,000 and received 100 free trades to be used within three months. I compiled a list of dividend increasing companies I buy when their price drops 2-3%, mostly dividend champions like KO, PM. Since the trades are free I make 3-4 small purchases through the day to average down as much as I can rather than one large purchase. My question is how would you go about using those free trades in order to fully take advantage of them? I’m I on the right track?

I absolutely love your blog, I have learned more by reading your blog and the comments than with any other book. Many thanks for sharing your journey to financial freedom and for taking the time to respond to the hundreds of questions.

Obet

A quick question. You don’t pay any attention to the price of the stocks that you are buying then? As long as the company is a company you want to invest in you buy them every month without paying any attention to the price? Or do you buy the “cheapest” stock in your portfolio every month? 🙂

Great article.

You simply have to cash flow your life and create a regular surplus of capital so that you’re investing in the ebbs and flows of the market- dollar cost averaging your way in over a long period of time.

It’s exactly what I’m doing, and I think the stock market is the best place for that.

When you become independent, if you can have a surplus of cash-flow, then you can reinvest it every month in order to reinforce the total cash-flow, whatever is the market, and even if you are making some mistakes with your investments (you will do). It is a virtuous circle: more cash-flow to get more cash !

Great article – i’ve been DGI for 4-5 years now and have seen many of my initial purchases double in value due to a combination of both capital appreciation and re-investment of dividends.

I know there will be those that will argue that you may be better suited for a better entry point and thus purchase more shares with the same amount of money, but having read many books on investing, this seems like market timing to me. That being said, if the market has a few triple digit gain days in a week, i may sit for a few days and see if the market comes back a little.

I heard you as a guest on a F.I. podcast (sorry, can’t remember which one) and i liked your comment / view that you really don’t compare your results to any particular index, primarily because you have a different gauge of success than an index – the index is looking at the total value of the stock compared to a given point in time in the past, where you are looking at how much income your portfolio is returning. I think that is an important concept for your readers to understand. In other words, you aren’t necessarily concerned with the daily value of your portfolio, you are concerned with the monthly / annual passive income generated by your portfolio.

Lastly, i’d like to hear your thoughts on using a home equity line of credit as the emergency fund, and investing the available funds to build a emergency fund into building the dividend portfolio.

“In that case, I’ve got bad news for you. The broader stock market – the S&P 500 index – has increased by 94.7% over the last five years. And they’ve almost moved in a straight line up, about as straight as stocks can go.

Maybe that means stocks have to correct from here. But maybe not. What I can tell you, though, is that someone who’s been waiting for a big stock market correction over the last five years to deploy capital has been doing a lot of waiting.”

I’ve been reading for about five months now, and I have been recommending this blog to a lot of people. I stopped reading this post after the above quotes.

2014-5 = 2009. 2009 . . . why is that so familiar? Oh yes, I remember now, it’s the year the stock market had a major correction. Oh . . . and when is the best time to deploy cash? Correct, when stocks are less risky, aka when there is a reduction in price! The past five years were the best time to deploy cash into stocks as they were less risky. Today, the market is at new highs. Should I be worried? Yes and no, overall, the market increases long term, the market has beaten new highs year upon year upon year. That does not mean the market will lose 30% today or even tomorrow. I would rather buy JNJ at 70 USD than 100 USD, it will get me more shares, increase my dividend yield and decreases the my risk of losing the principal if the company begins to sour. Buffet has said (and he is often right) today, the stock market is still in the range of “buy”, it is not in the overvalued range.

Graham has said there are two ways to intelligently invest, either save your money and wait for a recession or to dollar cost average. Buffet has said the same, as has Howard Marks. The more you pay for the stock, the riskier it is, not the other way around!

A cannon, located on earth, fires a cannon ball into the air at a 30 degree angle and for the first half mile it moves up in a straight line, about as straight as a cannon ball can go. Does that mean it hold that course forever?

Your “logic” or proof of point is laughable, it shows lack of mental effort to prove your point, I.E. why would someone hold cash in the past 5 years for a major correction when 5 years ago there was a major correction? THEY WOULDN’T. Only people who were too scared to buy would hold their cash.

He buys companies that have are quality companies that have a history of increasing dividends and the ability to increase dividends (significant earnings vs. dividend). In conclusion, he focuses on the dividend and the growth of the dividend, because he plans on living off the dividends (nice goal).Which is what I do too, though a little bit differently now. I am taking value into consideration also (even though I never plan on selling). I want to insure my capital gets the highest yield possible if I do in-fact have to sell.

Martin,

Glad you enjoyed it and found some value in it. That’s why I write. 🙂

$12,000 dollars is nice to have. No doubt about it. But that cash just sits there. It doesn’t grow all by itself. Doesn’t duplicate itself. On the other hand, cash flow can and does grow. And it flows and flows.

Best of luck finding the right opportunities!

Cheers.

Jos,

Right. Timing the market is just something that cannot be done, unless you possess a crystal ball that can predict the future. I’ve received quite a few emails over the last couple of years or so, especially over the last year, that indicated that I was crazy to continue investing. In the meanwhile, my cash flow has increased substantially, which provides me even more continuous firepower if/when cheaper stocks do become available. And as you state, it’s indeed a market of stocks. So I’ve yet to really search through all the merchandise at any given time and not find a value somewhere in the store. Value is relative and subjective, but cash flow isn’t. If your goal is to build enough cash flow to replace your expenses, then the work needs to be done on a consistent basis. 🙂

Thanks for sharing your thoughts. Couldn’t agree more!

Best regards.

Seraph,

I’m a slave driver as well! I’m pretty brutal. Those dollars don’t get much of a break out of me. 🙂

Yeah, that book is surprising in some ways. I recently had someone advise me that he wasn’t a big fan of the book. There are some passages that don’t paint him in a particularly good light, especially in regards to the family stuff. But there are only so many hours in the day, and ever activity competes with every other available activity. The more time you spend on investments, the less time you have to spend on other things. Such is life and the limits of our time. Hope you enjoy the rest of the book!

The movie was amazing. It was incredibly beautiful, although some parts were a little out there. Good stuff, though.

Thanks for dropping by. Hope you feel better!

Cheers.

Ville,

Haha. Lazy money. Money is indeed lazy if you don’t put it to work. It will just sit there all day long, doing nothing. 🙂

Thanks for the support! Glad you’ve been able to score some opportunities!

Take care.

Jason,

I hear you. I also anxiously await fresh capital. Investment ideas are never short in supply, but cash is. Which is really the whole point behind increasing cash flow. Cash is expended the minute it’s spent, but spending that cash on assets that produce growing cash flow gives you greater and increasing firepower in the future. 🙂

Thanks for dropping by! Glad you found some value in the analogy.

Best wishes.

Hey DM,

Listened to your interview on Radical Personal Finance, thought you did really well and I enjoyed it. I see a lot of the discussion posted in this post, I thought the analogies with the tree and fruit were great, liked the rebuttal on Warren Buffett, Steve Jobs, Coke, etc. I’m not a Dividend guy yet, but I will be looking to have a percentage of my cash flow in dividends(I’m real estate cash flow heavy) for FI.

Jason,

I couldn’t agree more. I generally do the same and deploy my cash as soon as it comes in. Its better to focus on cash flow rather than price, as long as, the equities you are buying are not overvalued.

B,

That’s a good question.

I generally trust management teams to make the right call there as far as cash goes, but I also don’t like companies that hold substantial cash on the balance sheet for lengthy periods of time. That gives management a lot of leeway in regards to the potential of overspending for poor acquisitions or just wasting the money, plus the money itself isn’t creating ongoing value for shareholders. And that speaks back to the point of paying a dividend in the first place. Giving management teams too much money just creates an environment where the decision-making process can be poor. I like solid balance sheets with low debt/equity ratios and high interest coverage ratios, but you don’t need a ton of cash to produce these results. I certainly like companies that are liquid, but too much cash is probably just a waste. So there’s a balance there.

Cheers!

Hey Jason,

You know how I feel about cash flow, I think increasing your spread is the most important financial concept one can learn. So I agree entirely that after your emergency fund is covered that your should be building your cash flow in some way. Despite the market being at all time highs, there are alot of individual stocks that seem provide excellent value. And anyone who can consistently add to their portfolio will be better off over the long haul as those stocks will now be producing cash flow.

Curtis,

I hear you. Put those suckers to work! 🙂

I don’t keep a lot of cash around. I generally have around $5k or so for emergencies, which is actually more than it used to be. And that’s because my employment/income situation has changed so much recently. I used to hold $2k or $3k and be completely comfortable. I suppose once I’ve been doing this for a while and feel a little more comfortable with my ability to earn income I’ll probably scale that emergency cash back down a bit and put the rest to work. I actually wrote about emergency funds a while back, and feel the same way as you. A bunch of money on the sidelines generally isn’t very necessary for most people.

Congrats on the success over there. You definitely know what it means to turn cash into cash flow, and why the latter is so much more powerful!

Best wishes.

FRD,

Glad you found some value in the article! 🙂

Thanks for dropping by.

Take care!

Obet,

Thanks for the kind words! Glad you’re enjoying the blog. I’m here to share, inspire, and learn. And the community we’ve built up is really wonderful. I think you’ll grow and learn a lot over time. 🙂

Those 100 free trades are completely free, so it’s up to you how you use them. I would probably make smaller investments, although there’s a time commitment there to constantly following the market and executing all these buys. So I might invest $500 or $600 at a time, rather than my usual $1,200 or $1,400. But I think there’s otherwise relatively very little value to be had there, especially since we’re not talking about an extremely large base of capital. Getting a slightly better deal on some of those trades over the course of just a few months will make very little difference for you over the long run, to be quite honest. But it’s also nice to be able to average in and get comfortable. So I’d say the psychological benefit is probably far more useful than any financial benefit, unless a substantial downturn hits the market over the next month or two.

Best of luck! Happy shopping. 🙂

Cheers.

I try to stay pretty close to fully invested. The most Ive really felt comfortable holding on the sidelines for a month ir two has been about $10k. But Id much rather get my capital working for me. The comparisons to Buffett never made sense to me bc the end goal is completely different. Most of us are trying to build up enough cash flow from our investments to become financially independent. Thats only going to work by investing capital. We dont have the luxury of waiting for once in a generation opportunities like in 2009. Wish I was investing then! Buffett runs a company who’s primary goal is investments. Plus hes one of the greatest capital allocators of all time.

Jake,

Thanks for dropping by!

Yeah, I get the value in comparing oneself to Warren Buffett, although the comparisons are generally apples-to-oranges. That being said, his habits and general philosophies can be replicated to a degree. But a young Buffett is more apt, even if it’s still fairly far off. I just found it interesting that the guy couldn’t get his hands on enough cash when he was younger. And he’s had a lot of cash come his way over the last 60 or whatever years, and almost all of it has been invested in fairly short order.

But to say that Buffett holds $X in cash and then compare that to your own situation is really just not of use/value. One guy is running one of the largest companies in the world and is on the back end of his career/life, while you might be a young investor still aiming for financial independence.

Best regards!

Martin,

I definitely pay attention to value. That’s why every stock purchase that’s published here has a section completely dedicated to value, after a fairly lengthy fundamental and qualitative analysis is performed. I don’t buy stocks if I think they’re expensive. I try to buy high-quality stocks that are fairly valued or better. That being said, I haven’t really run into a situation over the last 4 1/2 years where I haven’t been able to find at least one attractively valued stock out of the entire universe of stocks available out there. The stock market might be pricey at any given moment, but that doesn’t mean all the merchandise within the market is also expensive.

You may want to read some of my other content:

https://www.dividendmantra.com/2014/09/price-and-value/

https://www.dividendmantra.com/2014/06/why-investing-new-capital-during-all-time-market-highs-doesnt-scare-me/

https://www.dividendmantra.com/2014/05/if-i-were-starting-all-over-again/

https://www.dividendmantra.com/2014/02/separating-company-performance-from-stock-performance/

I think that should get you started. 🙂

Cheers.

Eric,

It’s indeed a virtuous cycle. More cash flow buys more stocks, which provides more cash flow. Even better, increasing dividends further boosts that cash flow. Keep it up and you find yourself financially independent one day. 🙂

Thanks for the support. Glad you understand the concepts laid out!

Take care.

tonystrauss,

I’m in the same situation as you. Some of the stocks I’ve bought have doubled in value. However, value is relative. So some are still good buys. Some are not. Really all depends on their current valuation. I don’t really look at whether they’ve doubled or tripled, but what they can provide for me in the future, most especially from a cash flow perspective.

Glad you heard the podcast. That was on Radical Personal Finance. It was a ton of fun and we covered a lot of topics over the course of the hour and a half. 🙂

Your last question is basically relating to taking on debt to invest in stocks. I don’t advise it. I certainly don’t see any harm in knowing that HELOC is available to you in case you were to run into a genuine emergency. However, investing in stocks isn’t an emergency, right? So that’s like investing on margin. Great stuff when things are rosy, but not so fun on the way down. I generally avoid it because it’s not necessary to achieve the type of financial independence I’ve laid out. And I’m always anxious to pay off debt, not incur it. So that’s a strategy that might work out for you, but it’s a risk that is, in my opinion, unnecessary.

Though, I did point out that a stock portfolio can provide for emergencies due to the ongoing cash flow it provides:

https://www.dividendmantra.com/2014/04/break-in-case-of-emergency/

Thanks for dropping by!

Best regards.

Mike,

Your comment is all over the place, and I’m not exactly sure what you’re saying. It sounds like you’re moving on, and that’s fine.

But you state that Buffett has indicated that the entire stock market as a whole (which isn’t something I generally follow, for the most part) is still in the “buy” range, and yet you’re also stating that you’d rather buy JNJ at $70 rather than $100. Well, I think we all would. But who’s to say if/when that will happen? I lack a crystal ball. Maybe you own one. If so, I recommend to use it.

Sounds like you’d rather time the market, which is something I don’t advise.

Either way, I wish you luck!

Cheers.

Steven,

Glad you enjoyed the podcast! I was hoping that would reach a new audience, and perhaps put a different spin on the strategy.

I actually missed an entire point behind the Steve Jobs discussion, and sometimes that happens when you’re discussing multiple points within one conversation. Ultimately, I was going to point out that Apple is now paying a dividend. And that’s probably because they just lack other opportunities to grow and perhaps the level of innovation may slow down, or they don’t need that much capital to continue innovating. So management is basically telling shareholders that they have enough cash now to do everything they need to do, and keeping the rest (what they’re paying in a dividend and spending on buybacks) would be wasteful. I forgot to point that out. 🙂

Thanks for dropping by. Hope you’re able to find some success in this arena if/when you take it on.

Best wishes.

Mr. Stock Fox,

“Its better to focus on cash flow rather than price,”

Well, I’m not actually recommending that. I’m recommending to focus on cash flow rather than cash. Price should be compared to value, and I always advise to pay attention to valuations. Buying an overvalued stock might not burn you if it’s a really high-quality company and you plan on holding for a long time, but buying at fair value or better is obviously the better choice, all else being equal. A cheaper stock increases your yield, which buys you more dividend dollars for the same capital outlay.

Thanks for stopping by!

Take care.

Kipp,

Definitely. Consistency is the name of the game. The stock market might be at/near all-time highs, but that doesn’t mean every stock within the market is also at an all-time high. If the stock market is a store, I’m generally checking out the clearance stuff out back, rather than looking at the pricey merchandise near the front window.

Best wishes!

I’ve been transferring money to my brokerage account every month, but only make purchases every other month. The more I invest at any one time, the less it eats out of the return of each share.

JC,

I hear you. I’m just about always fully invested. I want those dollars working for me, not the other way around. 🙂

And I hear you there on Buffett. To compare his desire to hold billions of dollars in cash when he already runs a $350+ billion company to your stock portfolio that needs to get off the ground and generate enough cash flow for you to become financially independent is really not appropriate. Once you’re actually financially independent, then you can probably be a bit more conservative with cash deployment. And Buffett has been FI for almost his entire adult life.

Thanks for dropping in!

Best regards.

Joel,

Right. Commission fees should be carefully considered. I’ve discussed that countless times, but I generally try to invest $1,400 or so at a time due to my commission fees being $7 per transaction. That limits my fee to 0.5%, which I feel is acceptable in the asset accumulation phase. Sometimes I’m a little lower, sometimes higher. But I try to stay within that range. Free trades also help.

Keep up the great work!

Take care.

DM,

Of course. I really couldn’t imagine it – unless all stocks were trading at P/Es of 25+ and have no movement volatility with deposit rates at a dividend yield level… but even then – dividend tax rates are better : )

Cheers to owning more little diggers to keep the dirt flowing. 2 month push, we can do it, lets roll.

-Lanny

Hi Jason,

I see you’re currently reading Snowball. That’s a great book. If you get the time after reading Snowball you should definitely read: The Essays of Warren Buffett: Lessons for Corporate America, if you haven’t already. Lawrence Cunningham took all of Buffett’s annual letters and made an amazing book out of them. The great part is its in Buffett’s words and not somebody else’s.

Thanks,

Frank

I definitely agree with you about not liking to have too much non-emergency funds laying about. Its much more preferable to make that money work for you and have it being utilized. $_$

I used to have a 12K emergency fund. I quickly realized that it wasn’t worth having all that cash sitting in a bank account because I could invest the money in a stable company like ED that rewards me with a handsome dividend every quarter. I’m very much glad that I invested that 12K when I did in order to lock in a nice YOC in several quality companies.

These days we do have an “Escape Fund” that will help us travel from one part of the world to another. A portion of it is in a CD, but the majority is in cash. Since we have just entered FI we are keeping most of it in cash, but once we get the hang of things I may invest it in some way (most probably DGI stocks, but there’s also P2P lending, which I haven’t tried yet).

Hi DM

First i want to congratulate for the website, it has become my favourite dividend investing blog i found so far , and i do read it every day. I am a hungarian guy living in Berlin and i started investing in october 2013.

This article about cash or cash flow really hit my week spot , because i am quite defensive with my portfolio and most of my money is in overnight deposits (62%) where i get ~1.2% interest ( i might cover the inflation with that ), my stocks are like 38% of my portfolio mostly blue chips from US and Germany. I invest monthly at least 1200 euros, but i’ve invested like ~5000 during the recent dip in the stock market. My problem is that i have 40.000 euros of cash which i am a bit afraid to put to work at these all time highs at the stock market, and i have to keep in mind diversification not only between sectors but between currencies as well ( 54% -US dollar, 46 % Euro for now ). I’ve been lucky that i’ve bought most of my US stocks while the dollar was weak and now all my US stocks are green :).

I’m planning to wait a bit and see if the ECB will do QE in europe , that might boost the market again .

Any ideas that you’d do differently if you had 60% of your net worth in short term deposits ?

Best regards!

Guys,

This meeting in May sounds like something I’d enjoy attending but

do you have to own shares of BRK.A or BRK.B to be able to attend the meeting as shareholder?

Thanks

Denis

Interesting perspective. So long as we’re talking about cash in an INVESTMENT portfolio, I think you’re exactly right.

In my investment accounts, I also hold little cash. I rarely have more than a few thousand build up, and even then it’s not sitting around for more than a month or two. Usually, once I hit the $2k mark, I’m ready to buy. I don’t feel that I’m a very good market timer, so I don’t really try; however, I do “bet” when I think there’s a good entry point and may stretch my budget and savings account to get into something I think is a good opportunity.

I think the mindset definitely changes when you’re in capital preservation mode vs accumulation mode… as well as the amount of “cushion” you have to absorb any surprise expenss.

Simply fantastic man! I’m just starting my dividend journey and so far just got $700 a year in dividend income but that sucker is gonna grow and it’s gonna grow big:D

Hi Zoltan,

About the 40k€, I would like to have your kind of problems 😉

Have you looked at the UK sotck market ? Other currency (pound), big companies with good yield (Shell, Unilever, HSBC, BATS, BAE, Diageo, GSK…). The FTSE 100 has a P/E around 13, far from a bubble.

You know that 25 years ago it was not possible ;)))

About timing the market, if Jason had to wait a major correction before to invest (because of euro crisis, russia, china, fiscal-cliff, fed issues…), well, he would still be working at the auto center, had 0$/month from dividends and the blog would be empty…

Frank-NY,

I’ll definitely check that out! I’m about 40% done with re-reading the biography, and I really wanted to go back over some of the earlier chapters. I think I skimmed too much my first time around.

Thanks for the suggestion!

Cheers.

DW,

Absolutely. Dollars are lazy. If you don’t force them to go out and work, they’ll just languish away. 🙂

Thanks for dropping by!

Take care.

Spoonman,

That’s great stuff there. That $12k, had you not invested it, would be worth even less now on the basis of purchasing power. Instead, it’s developed into a passive income machine all by itself. Good stuff! 🙂

The Escape Fund sounds pretty nice. I imagine that once I cross over the threshold, as you guys have, I’ll be a bit more conservative in regards to reinvestment to maybe fund some other ventures. Travel and philanthropy immediately come to mind, but it’ll really depend on what’s going on at that time. I hope you guys get good use out of that money and travel the world!

Best wishes.

zoltan,

Thanks so much! Appreciate the kind words of support. I’m so glad you’ve found a lot of value in the blog. 🙂

If I had 60% of my net worth in deposits like that I’d slowly deploy the capital in the most attractively valued dividend growth stocks I could find, while also being mindful of diversification. I probably wouldn’t deploy it all at once because I’m just not built that way, but I’d try to invest it over the course of 6-12 months or so. So I would simply tack that extra capital on top of the usual investments. If you’re usually investing 1,200 euros every month, I would simply increase it to 4,000 or so euros every month, slowly draining that extra capital dry. That’s how I would do it, but you have to find what works for you. In the end, I believe the focus should be on cash flow, rather than cash.

Best of luck!

Cheers.

Denis,

As far as I understand it, you don’t need to be a shareholder. You simply need a ticket, or “credentials” as they’re called. 🙂

Cheers!

Ravi,

We’re on the same page. I’m not interested in timing the market, although I do try to make the most of my capital in any given month by focusing on value, quality, and diversification. That’s simply being opportunistic and intelligent, in my view.

I agree that the mindset will probably change once financial independence has been attained. I mentioned that toward the bottom of the article, that the reduced necessity to constantly accumulate assets frees you to do other things. I would probably want a much larger emergency fund when I’m older, for instance, so as to account for unforeseen medical issues. I feel comfortable running on the minimum at 32, but I’m likely to feel a bit different when I’m 62 or 72.

Thanks for sharing!

Best regards.

I have tended to not keep much cash on hand either. I sometimes let some accumulate to reduce my transaction costs, but for most people I would agree they should just dollar cost average.

I keep even less in my investment accounts. I usually won’t sell something until I know what I plan on buying next.

Hi Eric

Thanks for the reply, i do own Unilever but the NV shares not the plc, i’ve been watching BP but i think i’ve made a good decision not to invest in it yet ( but 5.6 PE ratio looks cheap ). Shell, Diageo, Gsk and AstraZeneca are on my list, i will make some purchases in the comming months. My initial goal was to stay with 30% stocks, 70% short term deposits. I took a look at high yield corporate bonds but the 4-5% yield still doesn’t convince me to take the risk, some say it high yield corporate might be the next bubble ( carl icahn ) and if the US raises rates, the first to fall will HY corporate bonds.

And yes the 40K is a problem, first world problem i might say 🙂 i just look at the stock market charts from 2000-2014 there have been two serious crashes, who knows how i’d react when my portfolio will be -50%.

Vawt,

Right. I don’t recommend investing a dollar just because it comes your way. I generally let my cash flow accumulate into a sum of at least $1,200 or so before I contemplate investing it due to commission fees. Luckily, it doesn’t take that long for me to accumulate that much capital, so I’m investing fairly often anyhow.

Thanks for stopping by!

Best wishes.

I have no prob skipping an emergency fund if you are holding liquidable blue chip stock. Also timing the markets is tough yet everyone thinks they can do it. When people ask me when is the best time to invest I say yesterday and today is the second best time! You cant be afraid to make a move, if so stocks aint for u!

Will be super cool if u document your pilgrimage to our god Buffet!

We are on the same page Jason! Cash flow is always better then just Cash.. nothing can beat a waterfall of cash flow! I am also in the asset accumulation phase and I tend to keep investing all the available cash that I have. this ofcourse excludes a emergency fund I am keeping aside at all times.

should a major crisis happen (15-20% correction) only then I would consider tapping into this emergency fund to add to my portfolio. Hoping that thiss will never happen it’s just to guarantee I sleep well next to my lady every night. This emergency fund also ensures I can invest and enjoy life at the same time!

Credit card is my emergency fund. And in worst case scenario you can get loan against your stocks

A-G,

Everyone’s comfort level and needs as far as an emergency fund are different. However, nobody really “needs” a bunch of cash sitting around in an investment account. A case could certainly be made that that’s the better way to invest – stay extremely liquid for the downturns. But I look at it from a different perspective, which is probably more appropriate for those without huge portfolios already under control.

I’ll definitely take some pictures and put something together for the Omaha trip. Seems like a great town, and the annual meeting should be a dream come true. Really looking forward to going at least once in my life. 🙂

Cheers!

niko,

Right. That’s not a bad way to go about it. I have more than $10k in available credit, so I feel pretty comfortable that if something were to hit I’d be okay.

I keep a little liquid cash for emergencies, but other than that I invest everything else.

Thanks for stopping by and sharing!

Take care.

DDI,

Absolutely. You have to be able to sleep well at night. And knowing that you have liquid cash to cover emergencies is a great way to ensure pleasant dreams. But I’d rather create a “waterfall of cash flow” (I like that!) out of the remaining lake of cash I have for investments. 🙂

Sounds like you have a great plan together over there. Keep it up!

Best regards.

Jason

Love the collecting shovels analogy, and with regard to Warren Buffet, he doesn’t bother with shovels anymore, but just goes out and buys a backhoe to dig the hole in one go!

Like you I prefer to get my cash out on the streets and working hard for me rounding up dividends, and have never managed to sit on the cash for long, indeed I got a payout from my employer’s shares at the end of September and had invested it by 9th October (with hindsight been better to have waited, but I will pass the ex-dividend date on the shares I bought on the 9th October on Wednesday, if I had waited a bit longer I would have bought the shares cheaper, but missed the dividend.

As a dividend investor, I only consider four things:

1. Is the company producing reliable earnings?

2. Will the company continue to provide reliable earnings?

3. Will the reliable earnings allow it to pay a decent dividend?

4. Will the dividend payments increase over the next five years?

If I believe the answer is yes to all these questions then get te cash invested and start receiving the dividends.

Finally, how many people predicted on the 15th October that the market was going back up more or less to where it was at the beginning of the month in the next week? I bet you could count the number who did predict this on the fingers of one hand

Best Wishes

FI UK

Great post Jason,

I almost feel as though your speaking to me, Especially with the examples you have laid out and along with the given scenarios.

Right now I am actually sitting on a lot more cash than what I normally do, and truth be told it does pain me to leave it in my account doing nothing. And its hard to come up with justifications to not invest it. Although I stated I didn’t want to spend it until the right time I feel as though doing this route is causing me more anxiety than actually having it out working for me. (talk about first world problems eh?)

Either way I really do appreciate you posting this up because I’m starting to questions whether or not i really want to hold cash until the right moment comes along.

I still have yet to make an emergency fund, but as you pointed out my portfolio itself is my emergency fund. I’m a huge advocate of compound interest so i feel like a hypocrite not getting my money to start working for me ASAP.

This article indeed is very thought provoking!

Thank you for sharing

Ace

How much do you plan on spending for the trip to Berkshire meeting in 2015? I wanted to go too, but it’d cost me $200 for a round trip greyhound bus fare (the cheapest means to get there from GA I know of). Is it worth the cost, or isn’t it better to invest that money instead?

FI UK,

That’s a good point on the recent drop. The impossibility of timing the market is what I was pointing out in the article, using that most recent drop as an example:

“It’s like we recently witnessed just this past month. The Dow Jones Industrial Average fell by 1,000 points from October 8th to October 15th. 1,000 points. Do you let the cash go after 500 points? Or 1,000? Is the 1,000 the harbinger of better opportunities? Well, you had to act fast, because the DJIA bounced back just as fast – up by 1,000 points by October 24th.”

It’s just impossible to say when to let the cash fly, if you’re holding it. Hindsight is always 20/20, but it’s pretty tough in the thick of it to know the right moment.

Appreciate you stopping by and sharing your methodology. We’re pretty much on the same page, my friend. 🙂

Cheers!

Ace,

I’m glad you found some value here and perhaps had your eyes opened. I’m not saying anyone should just go and lay out all their capital in the stock market. Rather, I think one be thinking about why they’re holding cash, if they are. There are opportunity costs on both sides of the aisle, but I can think of no bigger opportunity cost than delaying freedom. And that’s exactly what I would have been doing over the last few years had I held on to a lot of cash.