How to Achieve a Retirement Income by Age 40

Did you know that one third of Americans are worried they’re never going to achieve a retirement income? Meanwhile, some weirdos out there, me included, are ‘retiring’ in their 30s. How do we manage to do this? Isn’t retirement supposed to be something that happens to you right before you kick the bucket, at the end of a long, strenuous lifetime spent working?

No.

I decided it wouldn’t be that way for me, which is why I managed to quit the 9 to 5 job I didn’t like at 32. Of course, just because I did it like that doesn’t mean that you have to do it as early as me. You might find my kind of plan too taxing. Maybe you’re one of those folks who likes to indulge a little while they’re young.

Or, you could choose to enjoy this kind of lifestyle for the rest of your life… Your call.

Image source: Benzinga

I’m not judging and I completely understand—even though my goal is to afford the kind of life I’ve always dreamt of later on, but keep it forever. In the meantime, though, I’m going to dispense some advice you might find useful, regardless of when you want to achieve that Holy Grail that is your retirement income.

3 effective strategies for early retirement income planning

If, like most Americans, you’re concerned about what you’re going to live on after you retire, I’m here to tell you there’s a simple way of understanding and achieving that kind of goal. You won’t have to go to extreme lengths to save up, nor will you be forced to give up on all the activities you enjoy now. You will, however, learn how to take a balanced approach to your spending, debt, and saving right now.

1. Know the kind of money you need

There are two specific figures we want to work out at this stage:

- The yearly income you will need after you retire;

- The amount of money you will need your investment portfolio to generate.

You can work out the second number after you’ve determined the first one. And, while this is not set in stone, the rule of thumb is that you need 80% of your working income in your retirement years.

Now, this all depends based on the kind of lifestyle you’re envisioning in your olden days. Perhaps you have good reason to believe you’ll be spending a hefty amount on health care. Maybe you want to downsize your home. Factor in your particulars and establish your needed income.

To calculate the size of your investment portfolio, forget about the conventional retirement income calculator. What you will need to bear in mind is the safe withdrawal rate—the point is to be able to take out 4% of your investment portfolio every year, use that money as income, and never worry about the fact that your will reach the bottom of the sack.

In other words, that safe withdrawal rate is what will help you determine the size of your income portfolio. We’ll assume that the 4% in question equals your need annual retirement income. Your portfolio will need to be 25 times the size of that amount.

Image source: Wikipedia

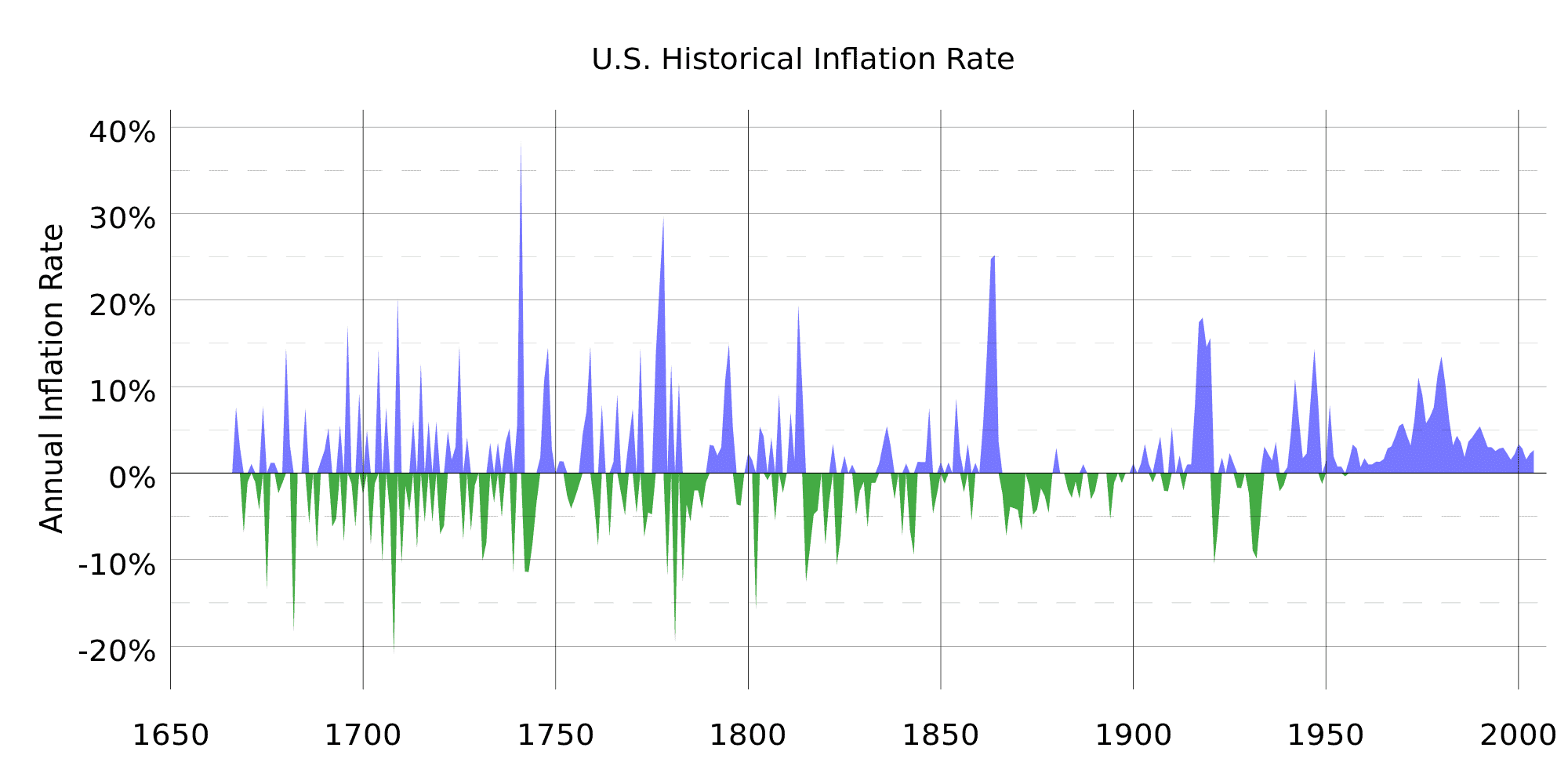

Don’t forget to also account for inflation. Of course, other than a magical crystal ball, there’s no other way to know what the inflation rate will do to your income. However, you can use tools to help you out, like the BLS inflation calculator available here. As an example, say you need a $1 million portfolio to retire at 50, i.e. in some 20 years’ time. By 2035, the equivalent of $1 million will roughly amount to about $1.5 million, based on past performances of the U.S. inflation rate.

2. Cut your expenses to the bone

Maybe you want to retire early, or maybe you just want to get out of debt. Whatever the case may be, all you need is some smarter way to save. This all starts in one place: the kind of money you need, in order to survive. How do you cut back on things? Start with whatever is not a necessity:

- Dining out;

- Vacations;

- Technology – drive an older car, don’t change your smartphone every 2 years;

- Relocate to save money.

That last point may seem bold, even for the most determined of savers, but it can really make a huge difference. That’s especially true for people living in very high cost areas, such as New York or San Francisco.

As for scaling back on luxury purchases, many early retirees have explained how amazing this actually is—contrary to the popular belief, that giving up on things you enjoy will reduce your quality of life. By cutting your expenses and saving them up in a low-cost index fund, you’ll be en route to actually taking over more control on your life.

It’s as easy as saving 50% of what you’re earning. Think that’s too hard for you? Write down all your expenses. Seriously, do it. Cut out anything you need to cut out until you start to see what your life would look like on 50% of your current income. It can be done—all it takes is a bit of creativity. The wisdom here is that, if you want to retire in 40 years’ time, you can probably get away with saving scraps—10-15% here and there. But retiring in 20 years’ time requires a bigger effort than that.

This being said, here are two ideas to consider:

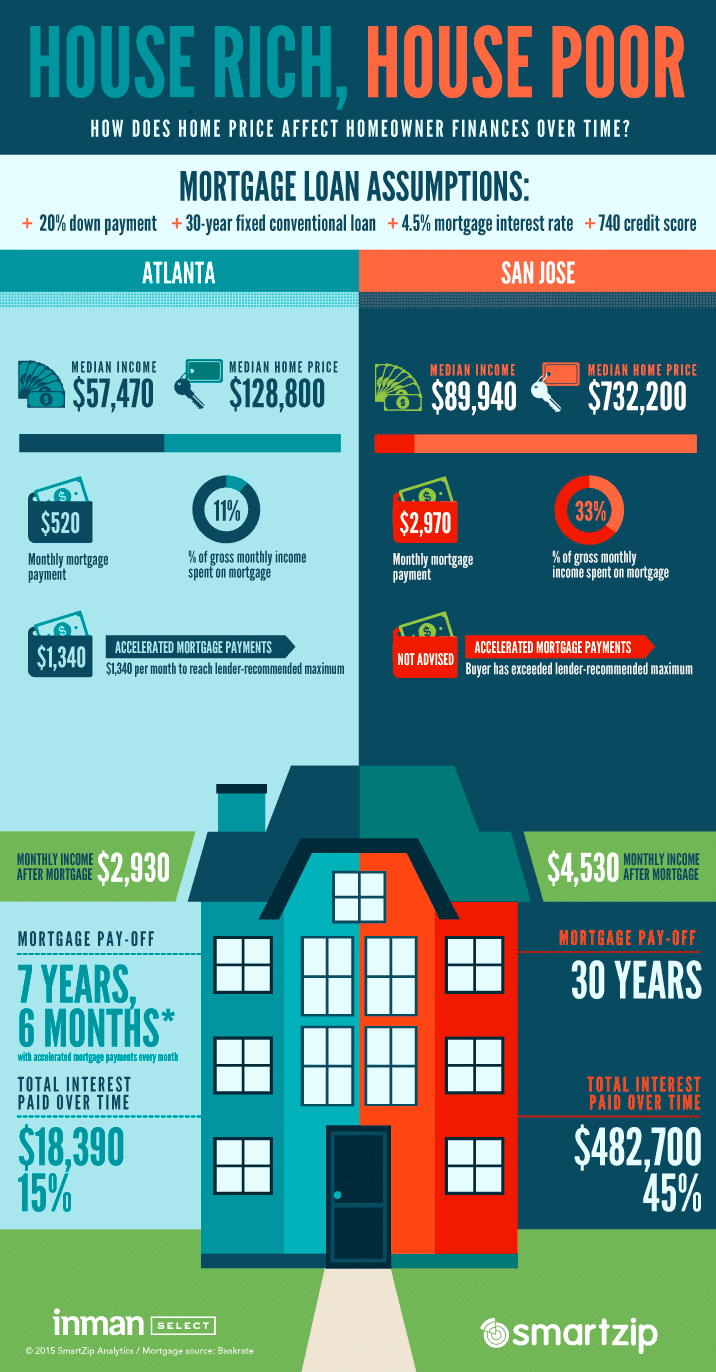

- Don’t be house poor. A lot of people make the mistake of taking out a mortgage for a home that’s beyond their means. They make their home the be-all, end-all of their lifestyle, without realizing how this basically has them stuck paying huge costs over a very long period of time. A bigger home, in a more expensive area, also brings along very high costs. If early retirement is your ultimate goal, try settling for a smaller home, which will bring along fewer expenses.

Image source: Smart Zip

- Set up your own retirement plan. You can contribute to your own IRA (or even a Roth IRA, if you’re eligible). Similarly, if you’re self-employed, you can set up a Solo 401k. The savings limit for your first year is a bountiful $18,000, i.e, 100% of your income, plus an extra 25% of your whole income. If you’re over 50, that $18k is actually an even more generous $24,000.

3. Don’t spend money you don’t have

This one has been repeated time and again, but it’s timeless advice, so it always bears repeating. One of the biggest traps you can fall on is spending money you don’t have, on things you don’t need. It’s a sure-fire way of sabotaging yourself out of an early retirement.

Keeping a Debt Emergency Fund around, just for that one time you’re going to borrow money is equally toxic. Make it a mantra that you will not accumulate more debt, because, as the popular wisdom goes, if you get comfortable enough living with debt, the odds are high that you will carry it into your old age.

Make sure to get rid of the bigger debt quicker, as you prepare for retirement. This means paying off your credit cards in full. If you’re only making minimum payments at the moment, you’re basically shooting yourself in the foot and making compound interest work against you, not in your favor.

Another option worth considering is finding extra employment, like a part-time job, a better paying full-time engagement, or even your own company. Whatever you do, make sure that all the extra money you’re making is going into your savings account.

How to create a smart investment portfolio for early retirement

Once you’ve saved up enough and are sure you can retire before it’s time, you will need some form of safety that your money is going to keep working for you, long after you have retired. While you’re at it, take a good look at this principle, and make a golden rule out of it:

The point to a happy retirement is to not run out of money.

Sounds reasonable, right? But how do you do this? How do you invest with safety at the top of your mind, while also making sure that you’re hedging inflation throughout your retirement?

Here’s how you don’t do it: by playing it safe. A zero risk investment portfolio isn’t likely to help you with this, because, at the rate things are going right now, it’s very safe to assume that inflation and interest rates are going to keep closely chasing each other. In other words, even if you keep your withdrawals at a bare minimum, your nest egg isn’t going to be worth that much by the time you retire.

So, what’s the solution, then? In a single sentence, the best way to approach your investment portfolio for an early retirement is to keep a good balance between risk and safety.

How to design the ideal portfolio for your retirement plan

The principle here is simple: create a good balance between a comfortable income and enough liquidity to see you through times when the market is behaving bearishly. To achieve this, you need to look at your investment portfolio as being made up of two discrete parts, with complementary, yet different goals:

- An equity part that is as diversified as possible. The problem with equity is, of course, volatility. To take this down to its bare minimum, make sure you’re diversifying this equity segment as much as is possible for you, while also keeping an eye out for long-term investments that will help you hedge inflation and fund withdrawals, thanks to high total returns.

- A fixed income part that can mitigate total volatility. With this part, you shouldn’t try to reach for high yields. All you need to do is keep close to the volatility levels of the money market—not lower the quality of your credit, and/or up your time horizon.

With both parts of your portfolio, you will invest for high total returns, not for income. Investing for income is a thing of the past, when dividend-paying stocks, preferred shares, generic bonds, and others were the norm. Yield reigned supreme at the time—and the eventual outcome was a portfolio low on total returns, yet high in terms of risk.

To be completely fair, those were different times, with better dividend and interest yields. However, nowadays, investment trends are pointing in a completely different direction. Investing is not about masterfully picking the right individual securities, but rather about building a strong portfolio, with high total returns, and intelligently allocated assets.

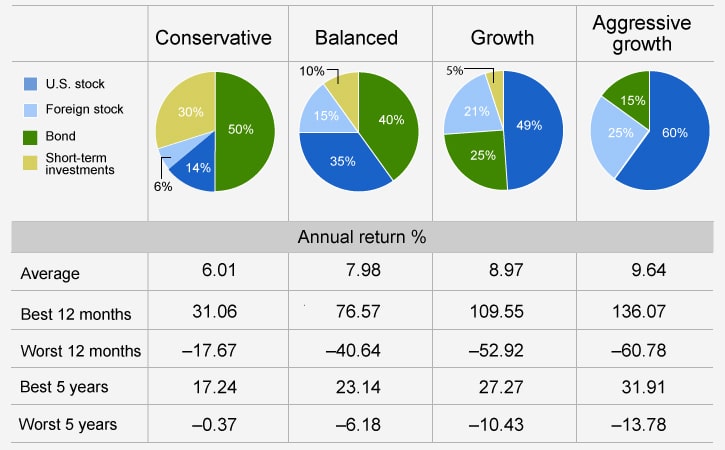

Image source: Fidelity

Avoid these 3 common mistakes when building your retirement income portfolio

Of course, we’re far from seeing a consensus on the best way to save for retirement among financial experts and rogue early retirees. Though trends will continue to emerge and some will swear by a certain option in favor of another, there are still two main schools of thought at play nowadays:

- Save the principal and live off your income.

- All income is good income.

After all is said and done, you, too, like your grandfather before you, will choose an approach to your investment portfolio that suits your time horizon, needs, and capacity for saving. However, while you’re at it, you might want to keep an eye out for these very frequently encountered mistakes.

Not striking a good balance

Living off the income alone might sound like a good idea… if you completely disregard inflation. Retiring with $1 million in 1990 and investing all the money in a 10-year Treasuries account might have meant living off $82,100 at the time. However, in 2000 your income would have reached $66,000 per year. In 2014, all the money left for you to spend annually would amount to a meager $27,000.

Forget the 60/40 rule

Between 1982 and 2012, for three entire decades, the U.S. witnessed a bullish bond market, in which a mix of 60% bonds and 40% stocks seemed appropriate. However, this is definitely not a good idea. Both the bonds and the cash markets are very volatile nowadays. Focusing on them alone would betray too much interest in living off income.

Don’t focus on high yields alone

It’s just as risky to pick stocks based on their high yields. While they may look good on paper, they might actually be concealing a company whose fundamentals are on the down and out. Companies that come with high-yield dividends have been known to be unable to support them with sufficient cash flows. In time, their dividends suffered.