The Joys Of Quarterly Estimated Taxes

Special note: I’m not a tax professional. What you see is a rundown of my recent experience paying my quarterly estimated taxes for the first time. As always, you should consult a tax professional for any tax questions or any specific tax situations.

Special note: I’m not a tax professional. What you see is a rundown of my recent experience paying my quarterly estimated taxes for the first time. As always, you should consult a tax professional for any tax questions or any specific tax situations.

No, that title isn’t sarcastic.

I actually view the fact that I have to pay quarterly estimated taxes for 2014 as a sign that I’ve made it as an investor. When your dividends are sizable enough to require paying quarterly taxes above and beyond what your employer withholds from your check I think that’s a good sign that your passive income snowball is definitely rolling downhill.

So 2014 is the first year I’ll be paying estimated taxes, and I thought I’d share the process with any other dividend investors out there that might be interested.

Paying Quarterly Taxes Is Surprisingly Easy

For all the complexities that exist within government – especially the IRS – paying estimated taxes is refreshingly simple. The process itself was actually quite easy. Meanwhile, figuring out how much you owe and remembering to actually pay might be a different story.

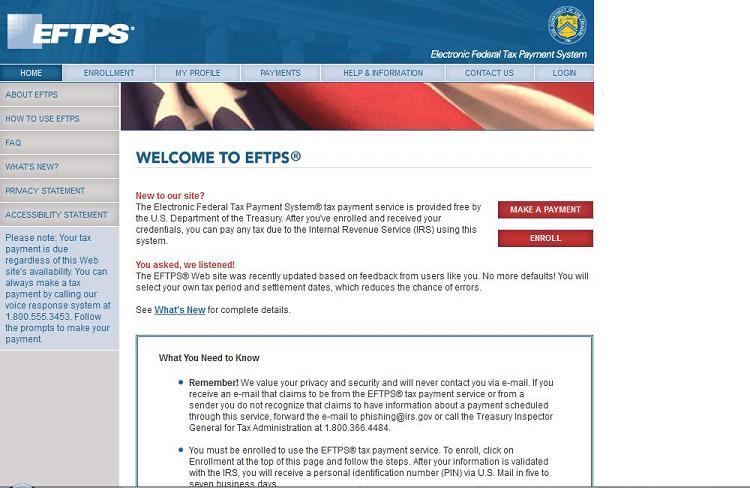

The first thing do do is head over to the Electronic Federal Tax Payment System (EFTPS for short) website. The IRS allows you to pay online, and that’s what I recommend doing.

You’ll then want to enroll if this is your first time. By clicking the little “Enroll” button near the middle right of the screen you’ll be taken to another area of the site that will allow you to enter some personal information about yourself. Here, you’ll enter your taxpayer and contact information, as well as your bank info. Unfortunately, it won’t be quite that easy after you’re done there. As a security mechanism the IRS will actually send you a PIN and enrollment number by snail mail to make sure you are who you say you are.

Once you receive this information by mail (it took 5 business days for me) you’ll then use the PIN and enrollment number to finish setting up your account. To do so, you’ll want to click on the “My Profile” tab near the top of the page, then “Need a Password” on the following screen. Choose a password and input the information the IRS sent you. Once you do so you’re in! Voila. Really easy stuff.

Once you’re in you can can make changes to your account like your profile or payment information. Once you’re satisfied with how your account is set up the only thing left to do is to pay. To pay you simply click the “Payments” tab near the top of the screen on the main menu bar and then follow the prompts to pay.

It’s really that easy.

Now The Hard Part – Figuring Out How Much You Owe

However, like I said earlier the harder part will be to actually figure out how much you will owe. For this, the IRS recommends using worksheet 2-14, which you can find HERE. While this worksheet is useful for those of us who make income from self-employment sources that have no outside withholding, dividend taxation is actually rather simple.

First, you’ll simply want to figure out which federal income tax bracket you fall in. I’m not going to delve too far into this, because that would be beyond the scope of this post. But once you figure out which federal bracket you fall into figuring out your tax percentage on dividends should be relatively easy.

For the 10% and 15% tax brackets qualified dividends are taxed at 0%. For the 25%, 28%, 33%, and 35% federal tax brackets qualified dividends are taxed at 15%. If you’re one of the lucky few in the 39.6% tax bracket you’ll be paying 20% on qualified dividends. Ordinary dividends are still taxed at your marginal rate.

For example, if you’re in the 25% tax bracket and you’re going to earn $7,500 in qualified dividends during the year of 2014 you’ll owe $1,125 in federal taxes. You would then simply divide that by 4 – because you’re paying out four quarterly payments. That gives us a sum of $281.25. So you would send in four equal payments of $281.25 to the IRS through the EFTPS this year.

It’s important to note that there are time restrictions on this. You must pay the first quarter’s estimated tax no later than April 15th for income earned from January 1 – March 31. The second quarter deadline is June 15, third quarter is September 15, and then the four quarter’s cutoff date is January 15 of the following year.

Paying Quarterly Taxes Is A Good Thing

While this all sounds like a bummer, I actually view the fact that I’ve reached the point to where paying quarterly estimated taxes is necessary as a good thing. As always, having a large tax bill is usually due to having a large income. I could go back to the days in my early 20s when I always got a tax refund in the spring because I never made much money, but I think I’ll stick to the situation I’ve built for myself now. Paying quarterly taxes due to dividend income means your dividends have grown to the point to where you actually have to manage that snowball. Folks, that’s a good thing! It means it’s turning into a monster. A cash monster. Congratulations, you’ve arrived!

So I just sent in $700 for my first quarter’s estimated taxes. Although this is much more than I expect to pay in taxes for dividend income, I am also receiving online income that I have to account for. As such, I sent in what I hope will be enough to cover any outstanding liabilities for both my dividend income and online income.

You Can Avoid Quarterly Estimated Taxes…For A While

Now, you can avoid quarterly taxes through a few different methods. What I’ve done over the last couple years is make sure to boost my withholding at work toward the end of the year to make sure I paid more than the prior year. Generally speaking, as long as you paid more in the current tax year than you did in the prior tax year you can avoid any underpayment penalties. Also, you’ll generally avoid penalties if you owe less than $1,000 above and beyond what was withheld or paid during the tax year. Furthermore, you’ll generally avoid a penalty if you paid at least 90% of owed taxes for the tax year in question. For instance, I owed $2,777 for the 2013 tax year because of my dividend income and online income, but I made sure to pay more in 2013 than I did in 2012 by having my employer withhold a little extra in December. Thus, I was not charged any underpayment penalties.

However, I owed quite a bit this year. And with my dividend income growing at a substantial rate I knew I couldn’t game the system much longer. So this year I decided to bite the bullet and actually pay the quarterly estimated taxes. And to my surprise the whole process was astonishingly easy. I hope that by paying out more every quarter I’ll owe much less come tax time next year.

How about you? Paying quarterly estimated taxes? Do you find it difficult?

Thanks for reading.

Photo Credit: bplanet/FreeDigitalPhotos.net

Jason you’re probably one of the few people who enjoy the act of paying taxes. I’m leaning towards calling you a masochist. 🙂 All joking aside I admire your positive perspective on the matter. It is indeed a nice problem to have and does show that your actions have brought you to a different financial position than where you were a few short years ago. Congrats man!!

I’ve had to make quarterly payments for a while now from online income and dividend income. At times I’ve used a credit card to make these payment (through the IRS website) just to qualify for large cash back rewards that are tagged along with a big spend requirement. Some cards offer $500 cash back which can make the fees worthwhile.

The EFTPS method is very simple as well and it’s what I usually use.

DM,

Sometimes the IRS can be surprising that they get things right. EFTPS is a good example of this. So is Where’s My Refund. In fact, they are improving a lot of their systems to produce faster refunds and reduce fraud. The real problem as to why taxes are such a burden is the lawmakers. I got a big refund this year so no estimated payment for me yet. Need to keep increasing those dividend purchases!

-RBD

While I wish that tax rates were lower, I appreciate that my tax bill is high since it means I have a large income. Quarterly taxes seem like a pain just having to keep up with it throughout the year instead of just once a year, but I guess it’s a lot better than the alternative of having a huge tax bill come the following year. Thanks for the update on how quarterly taxes work, I think we might forego quarterly taxes this year but I’m sure next year it will be pretty much necessary. If you happen to start earning significant income from a side job or dividends after the 1Q payment, can you start up the quarterly taxes then for the last three quarters or does it have to be all or nothing?

Would putting 0 deductions/exemptions on your W-4 be enough to get a little extra federal tax withheld?

I agree that when you make more money, you end up paying more in taxes. I would much rather earn $500K and pay 39.60% than earn $10,000 and pay almost no taxes. However, I also try to minimize taxes when possible.

The total amount of taxes I am paying every year is equal to the amount I can reasonably live off of. That’s why I am trying to minimize “tax waste” in my accumulation phase.

Good luck in your journey!

DGI

Wait, doesn’t the IRS charge you a transaction fee if you pay by a credit card?

This is something I hadn’t even thought of before. This year is actually the first year I’ve had to cut the IRS a check. Not an enjoyable experience, but with about $4000 in dividend income and $2000 in options income I should probably feel happier about it. I’ll have to look into either bumping up my withholdings at work or seeing if my brokerage account can start withholding some of my dividend income.

Ah, just saw the part where you mentioned the online income. I can see how the extra withholding is probably not enough. It probably is less confusing to just withhold the normal amount at work and then pay estimate amounts quarterly.

I agree with you about the disguised blessing of paying taxes. I owed a little over $1K this yr in total taxes (fed/local) when I filed. It sucks to know that amount will be drafted from my checking account in a few weeks, but it’s also (some) consolation that I only have to pay due to making a good income last year.

Keep fighting the good fight! I love your point about paying nearly 0 taxes on dividend income once you’re independent. Hopefully things don’t get too much worse, since there was a time until around 10 years ago when dividends were considered ordinary income and not subject to preferential rates.

I started running into the same issue last year! I lowered my W-4 exemptions from 2 to 1 to get an extra ~$1K withheld from my salary so I don’t run into as big of a bill come tax time. Too bad I only started doing that in November.

I’ll see if it works out better this year. Good and bad, but I hope one day when I have a family and kids, I can write 0 exemptions even though there should be 3-4! At least that will make me feel better about how much money I’m making from rentals/dividends!

Instead of paying estimated taxes, I just tweak my W-4 at work. I fill in zero “0” allowances. I also fill in an additional amount of money to be withheld from each paycheck (Line 6 on the W-4 form.) That way, I get to spread out paying taxes for my dividends and rental income, over the course of the whole year. That works for me, and I avoid having to deal with making any extra estimated payments or remembering the amounts of estimated payments, etc. It’s all withheld from my “wages” at work, and all appears on my W-2.

Congrats on paying quarterly taxes. That sounds bad but it just shows how well you are doing. It’s my first post here. You are truly an inspiration. I hope to get to where you are someday. Keep up the great work.

BTW, how do you feel about ARCP and GE recently declaring they will be spinning off a portion of their company? I’m thinking of starting a position in both. Do you think it’s better to buy before or after their spin off?

Thanks again.

The Stoic,

Haha! I definitely don’t enjoy paying taxes. But if it’s between paying taxes because I’m making a decent income and not paying any taxes because I’m making too little, I’ll take the former any day of the week. 🙂

And you put it succinctly: It’s a nice problem to have.

However, I’m looking forward to the day when my overall yearly tax bill is low because most of my income is coming in via dividends. The snowball is rolling faster and faster now.

Cheers!

DGI,

I couldn’t agree more. Typically, a big tax bill comes because you’re just plain making money. However, at the same time it makes sense to minimize them as much as possible. Every dollar not paid in taxes is another dollar to invest. And we all know how that can work out over a long period of time.

And I’m in the same position as you. It sucks to know that my tax bill alone could support my current lifestyle. But it just serves as motivation to keep doing what I’m doing. 🙂

Best regards.

Zach,

I’m not aware of the ability to pay via credit card through a different site. EFTPS requires bank account information, unfortunately. It would be sweet to collect some credit card rewards for tax bills!

Do you have some more info on that?

Cheers!

RBD,

The IRS can indeed be surprising at times. However, they have a long way to go before anyone’s a fan of how they generally operate. 🙂

Keep up those equity investments and you’ll be seeing a bigger tax bill in no time!

Best wishes.

JC,

I’m pretty sure you can’t send in just three payments. At least, not from the way I understand it. Maybe someone who’s a tax expert can chime in, but from everything I’ve read it must be four equal payments.

In that regard it kind of sucks, because if you have a really strong second half of the year and didn’t start paying estimated taxes in the front half you’re kind of screwed.

Best regards!

Ravi,

I already have my exemptions set to 0 at work. This past year I had my HR department withhold even more than that, but it’s a pain for them to keep resetting my tax info. It’s easier for me just to send in quarterly payments and forgo having to have my HR department go through the rigmarole. I was going to have to pay quarterly taxes sooner or later, so many as well educate myself now.

I’m not all that worried about dividend taxation changing. Regardless if the preferential taxation changes I’ll still be living off little income in early retirement, so my overall rate will be low no matter what. I could be wrong about that, but any extra income would just be icing on the cake. 🙂

Congrats on having a strong 2013 for income. That’s the name of the game!

Take care.

My FI Journey,

Hey, long time no see. Hope all is well.

I hear you. It’s certainly never fun to cut a check, but if it’s due to making a significant income then I can be okay with that. I’m also okay with it knowing that my exposure to high tax bills will be a relatively short period of my life.

Best wishes!

R A,

That’s a great way to do it as well. Thanks for sharing!

I also claim 0 allowances on my W-4, and for the last couple of years I’ve had my HR department withhold a little extra toward the end of the year. However, it’s getting to the point where that’s going to be too cumbersome. The quarterly estimated tax process, for me, is easier then having to go through my HR department at work and have them file paperwork for me.

And once I no longer have a regular job I’m going to have to go through the estimated tax process anyhow, so may as well get familiar with it now. 🙂

Thanks for stopping by!

Best regards.

Richie,

Thanks for the kind words! And congrats on starting a blog and starting your own journey. Glad you had your “epiphany”. 🙂

Generally speaking, spin-offs do very well for investors over the long haul. In light of that, I would want to be an owner before each of these companies spin off parts of their business.

Best of luck!

Take care.

Once a spinoff is announced, it should (in theory) be priced into the stock immediately… or at least within a few days once the investment community estimates how good/bad it will be.

Ravi,

The key part of what you said there is “in theory”. I don’t prescribe to MPT, and do not believe the market has any regular ability to correctly price all stocks. If I did I’d simply buy a few index funds and be done with it.

Cheers!

Welcome to the Quarterly Income Tax club. I also am required to join this year with a $600 dues payment quarterly. I don’t like it but as you say it is only because I made more money this past year. In past years my taxes were covered by my previous employer withholding taxes from my pension. Now however my RMD from my IRA has almost doubled and put me over the top of what my withholding has covered. Last year was a great year for us in the market so now it is time to pay the Piper.

I had never heard of quarterly estimated taxes before. Once again you have educated me on the world of finance. Keep up the great work!

Regarding paying tax bill with CC you can but the processing fee I believe is 2.49% of your bill basically wiping out your credit card reward. The Points Guy has a good post on it – http://thepointsguy.com/2012/03/does-it-make-sense-to-pay-taxes-with-a-credit-card/

Just go to IRS dot gov and go to payments. There are options there. It is true that there are fees when paying with a credit card however it can still be worth it if you are working towards a huge credit card signup bonus that requires big spend.

True, but sometimes you can still make a good amount and still pay very little in taxes. For example, you can make $150,000 and pay $150 in income taxes:

http://rootofgood.com/make-six-figure-income-pay-no-tax/

Gotta love all the crazy possibilities with the US tax code.

Good ol’ quarterly tax payments! The price of making loads of cash! In my previous job, I saw so many clients make tremendously large tax payments. Most people don’t realize the beauty of paying a ton in tax is generally a boatload of income. I try to minimize my own burden, but realize, with some level of happiness, that the more I pay, the more I’ve made. For you, your rapidly increasing online income will be the biggest driver towards your future tax burden.

Thanks for the advice, DM. Our situation is such right now that we don’t have to pay quarterly taxes. I think we meet one of the conditions you listed.

I look forward to the day, sometime in 2016 (for the 2015 tax year), when we pay almost nothing in federal and state taxes. That’s why I haven’t bothered getting an online account with the state or the IRS, because I strongly believe I won’t owe anything for the next 5 years.

In the long term, 5-10 years from now, I think I will look into paying quarterly taxes. The nice thing about doing that is that you won’t be stuck with a huge bill come tax time.

Hi Travis,

I am maxing out 401K, SEP IRA and Roth IRA to minimize tax waste. I get deduction on 401K and SEP Ira today, and when I retire, my tax income will be in a lower bracket, so I will slowly convert to Roth IRA and pay little to no taxes on the conversion.

Check this series:

http://www.dividendgrowthinvestor.com/2013/10/my-retirement-strategy-for-tax-free.html

Plus, do not forget that at certain levels qualified dividend income is tax-free ( 46250 for singles, 97500 for married filing jointly)

Travis,

Great example there.

I don’t have access to many of the plans that Justin over there does, but good for him for maximizing every opportunity available to him. However, I would note that some of those taxes are simply deferred to a later date, and how much he may have to pay will depend on a lot of factors.

Thanks for stopping by and sharing that!

Best regards.

Bob,

I’m with you. I hate paying out any money at all in taxes, but I understand the necessity for them. Furthermore, I’m comforted by the fact that this was my biggest tax year ever due to also my biggest income year ever. I’ll gladly take the two of them hand in hand any day of the week.

Congrats on also having a fantastic 2013!

Best wishes.

Gareth,

Glad you found something of value here! 🙂

This information isn’t necessary for everyone as many people don’t need to worry about quarterly estimated taxes. Furthermore, everyone’s tax situation is unique. However, I thought it was a good overview of quarterly taxes and how to initiate them if necessary.

Cheers!

W2R,

Couldn’t have said it better myself.

The more you make, the more you pay. Or at least that’s how it generally works.

And I’m with you: I try to minimize mine where necessary, but my biggest victory in this department will be retiring from traditional full-time work early. By way of this action I’ll be avoiding a ton of taxes that I otherwise would have paid for decades.

And I agree with you in regards to the online income. This will very likely be my biggest tax burden when I’m financially independent. However, it’s a burden I’d be glad to have. 🙂

Thanks for the support.

Best wishes!

Spoonman,

That’s awesome that you’re forecasting an almost tax-free life for the next five or so years. That’s the name of the game right there. Fantastic!

The online income will likely keep me from living almost tax-free once I’m financially independent, but I’m certainly okay with that.

If you ever do need to pay out quarterly taxes it’ll only be because your dividend income has grown leaps and bounds. And that’s not a bad thing! 🙂

Cheers.

Good point. I suppose the assumption of investment theory typically is MPT, but that’s more of an idea for generating the greatest total return. Dividend growth investing is actually not focused on total return, rather on free cash flow growth.

In this case, I meant that simply buying before/after the actual spinoff date shouldn’t (but may…) make a big difference. The real opportunity is if you disagree with what the market is doing to the stock. Especially if they are beating it down further than it deserves and a buying opportunity has presented itself.

I usually don’t try to do contrarian event investing. It actually works great, however, it requires you to be constantly dialed into a lot of stocks and news and I just don’t have that kind of time. I wish I did, though. Maybe once I’m independent I can be sure to dedicate at least a few hours a day on it 🙂

I’ve had good luck with spin offs COP with PSX and KRFT with MDLZ. I’m looking forward to the others. I already own GE and plan to own ARCP soon.

I know this is beating a dead horse, but with this post it bears repeating….why not do a traditional IRA? It will give you a tax break, it can be self directing, it will only be a small percentage of your current investing capital and drumroll please…….you can convert it to a Roth when you become FI and are in a lower tax bracket guaranteeing tax free income for life (until congress changes the rules).

I can only imagine having the dividends, that are thrown off in my ROTH IRA, being tax free.

Let’s admit, when you finish up at 40, eight years away. You would only have about $45k plus growth so we’re not talking about having to convert a ton of cash. But imagine having that $45k throwing off tax free dividends thereafter.

Who knows with the online income growing you could do a sep-IRA?

I actually see some benefits in paying taxes up front – sort of (although I hate paying taxes at all). Your year end will be easier to deal with. It looks like that my account will be quite successful this year (2014) too, so, I might fall into the same category as well.

And, the next thing is, you now can really consider your investing a business 🙂

I hate quarterly tax estimates. Try running a farm. I somehow have to predict my income for the year, when the prices of commodities change daily. Two years ago, corn was over $7.00 a bushel. Last fall, it was around $4.00 a bushel. When you’re producing 10’s of thousands of bushels of corn, a $1 a bushel difference makes a huge difference to your bottom line. Oh yeah, and not to mention that I spend $50-75k each spring before I see a dime in the fall.

Hi DGI,

Awesome! Looks like you have the tax game figured out. I thought I was doing pretty good until I came across Mad FIentist (via JLCollinsNH) and his Retire Even Earlier post. That opened my eyes to a whole new world of possibilities with the Roth IRA conversion ladder.

I would suggest you look into the advantages of a Roth IRA. You don’t get a current deduction for making contributions, but all of your dividends and capital gains accumulate free of tax as long as you keep the money in the account until you reach 59 & 1/2. Once you’ve had the account for 5 years, you can actually draw out amounts up to your contributions to the account tax free. If you go beyond that and draw into the earnings, those would be taxable, again only if you have not yet reached 59 &1/2. Since you are limited to $5,500 contributions per year, you should still have ample resources to draw income should you retire early (as I know you will).

What exactly is the threshold for having to pay quarterly estimated taxes?

Great post! Specially about taxes, something that is a key part of big portfolios and it’s hardly ever mentioned!

For now, I am being able to be tax free because I am investing small enough amounts that I can use the tax-free wrappers. I believe the equivalent in the US is the IRA. Eventually, I hope to have to take care of my taxes one day as well.

Best wishes and may your income taxes be ever increasing!

Search “IRS underpayment penalty” and you’ll get a link to the tax code. Each year, if you underpay your federal obligation and don’t meet those criteria, you can be fined/penalized.

Now that you have business income (from the blog etc) you could look into starting a retirement plan for yourself, either SEP IRA or better yet a solo 401k. I realize that tax deferred savings vehicles haven’t been a part of your plans but consider that rather than paying taxes now on your business income you can instead invest the money and let it compound, paying the taxes later when you ER at potentially a 0% rate (or no more than 10-15%). It would be a great place for your REIT and other dividend payers that are taxed at income tax rates rather than dividend rates.

My plan is to live off of savings balances early in retirement (thus having very little taxable income) and rolling over small portions of my tax deferred accounts into a Roth IRA. After a few years most or all of my retirement balances should be in that account which can be withdrawn tax free in retirement (and contributions can be withdrawn without penalty prior to age 59 1/2).

I’ve lucked out so far and have avoided quarterly payments. But I love your attitude on the matter: it really is a great problem to have.

ed69,

I don’t think it’s beating a dead horse. Maybe other people might get annoyed at the constant suggestion, but I actually appreciate that others are out there looking out for me. So thank you for that. 🙂

I’ve admitted that a Roth makes economic sense, and I’m leaving money on the table my not using one. However, I still think it’s a relatively small amount of money, as you rightly point out.

Furthermore, if I’m able to gain financial independence even before 40 I will. If I can retire early by, say, 38, then that’s what I’ll do. Every year that’s knocked off my journey makes retirement accounts less sensible. However, if I’m not able to retire by 40, and my journey is longer than expected, then it could be said I made a mistake.

But we’ll see. My victories and setbacks will be documented!

Best wishes.

Martin,

I hope 2014 will be successful enough to put you in a tax predicament. That’s a good spot to be in! 🙂

Best of luck with your investing this year.

Take care!

LR,

Ouch!

That’s a rough spot. I can certainly understand how frustrating that must be. Sorry to hear about that.

Even for me, it’s difficult to predict how much I should pay in quarterly estimated taxes because I don’t have a clear idea on exactly how much I’ll make in online income this year. I did my best, and I feel comfortable with that.

I’m guessing you must just overshoot your taxes so you don’t have a big underpayment penalty the following year? I’m guessing that’s the only way to do it. Rather unfortunate. I wish our tax system was simpler.

Thanks for stopping by and sharing!

Best regards.

Thomas W,

Ravi was correct. There isn’t really any “threshold” for paying quarterly estimated taxes. You simply have to avoid underpayment penalties, which can be avoided through any of the steps I laid out in the article. You don’t have to pay quarterly estimated taxes to avoid these penalties, but sometimes it’s necessary and/or easier to do so.

Best wishes.

DividendVenture,

Thanks so much for stopping by.

And good for you for taking maximum advantage of tax-advantaged accounts over on your side of the pond. I would so the same if I wasn’t on such a rather unique journey.

Cheers!

DB40,

While the quarterly payments are easy to pay, I’d certainly not hesitate to avoid them if possible. That’s what I’ve done for the last couple of years, so good for you. 🙂

Paying a bunch of taxes isn’t fun, but I’m comforted by the knowledge that my exposure to big tax bills won’t be for a very long period of my life. In the meantime, I’m happy to pay knowing that it’s a side effect of having a substantial income.

Best regards!

Steve,

Sounds like a pretty good plan there! Good for you for being in a pretty good position. I know that requires a lot of hard work to put yourself there, so congrats.

I’ve dismissed the idea of using traditional tax-advantaged accounts for a number of reasons that I’ve explained before, but that’s mainly because of my unique situation. For most others, I highly recommend them.

We’ll see how it all works out for me. My ideas, good and bad, will prove themselves out here on the blog.

Thanks for stopping by!

Cheers.

Hm, while ur on the subject of the niceties of the IRS: I paid penalties and interest for the past couple years or so for not filing quarterly, and it wasn’t much, most likely made more money by investing the difference in that time period. Have you done a study on the profitability going that route?! Keep in mind I filed on time and paid all the yearly tax payments when they were due.

Randy,

Haha! I guess the IRS is nicer than I initially thought? Too funny.

It’s hard for me to calculate what would come out better because I’ve never paid underpayment penalties, and it’s a vague subject. I know the amount you pay is based on prevailing interest rates, how much you underpaid, and for how long the money was owed. You could very well be right on investing the underpayment amount and paying the penalty later, but I guess I’d rather err on the side of caution anytime we’re talking about the IRS. 🙂

Thanks for sharing that. Glad they didn’t hit you too hard!

Best wishes.

Jason,

I’ve read your post about not using tax advantaged accounts but have you though of maxing out your Roth IRA. The reason is you invest in your taxable account with after tax dollars, in a Roth it’s the same thing but your dividends are tax free. Since you plan to live only on your dividends after five years you can “withdraw” your principle which is really the dividends you’re going to live on tax free.

Ex: You have $150,000 in a Roth IRA with a dividend yield of 4% You had contributed $100,000. You can withdraw $6000 tax free while you dividends and principle continue to grow. In 15 years you’ll hit the “principle” cap but by then you’ll be near the withdrawal age. The benefit is a part of your portfolio will not get a 15% tax hit on an annual basis, which frees up even more capital.

Just listened to Kraig’s new podcast, glad you guys are back even if only for a couple of weeks. Also you need to get yourself on the list!

http://rockstarfinance.com/blogger-net-worths/

I think once you “retire”, or whenever you start having a small amount of earned income that you are below the 25% tax bracket, then you pay 0% on qualified dividends.

Even if tax laws change and dividends become ordinary income, then it would have to be a LOT of growth before hitting the 25% marginal bracket, in which case most income would be at 10% or 15% anyway.

I do agree with you though, and in my own portfolio I’m trying to mix in some investments in a Roth and some in a taxable account. If I could do it over, I would have put more of my high-yielding stocks in a Roth since they are the least tax efficient. Oh well, you live and learn. Hopefully in 5 years with all my added investments, the amount in my taxable account won’t be significant so overall I will have a better tax mix.

DM,

Thanks for the article about quarterly taxes. I unfortunately was hit with a tax nightmare trio this year: I overpaid into my 401k in 2012, got a large 1099, and of course dividends. The net result was an additional $21,000 in taxable income and a $9,000 tax bill. I’m not exactly sure what the IRS rules are, but I believe there is an underpayment penalty that can result. I will look into raising my witholding taxes or maybe start paying quarterly like you.

Thanks again!

Charles,

Thanks for the suggestion there!

I don’t use a Roth because my dividend income in early retirement will most likely be tax-free anyhow since I’ll be living on less than the threshold for taxation. At least, that’s on qualified dividends. REITs will be taxed at my marginal rate, but, again, with a low overall income base I’ll be paying very little no matter what.

However, if I were on a longer journey I’d be taking maximum advantage of tax-advantaged accounts. But the amount I could put in a Roth between now and early retirement would only be $44,000 based on the max contribution and how many years until I plan on living off of my dividend income.

What can I say? I’m an anomaly. 🙂

Cheers!

Shane,

Thanks so much! Glad you enjoyed it. 🙂

Kraig contacted me not long ago to tell me he started up a new podcast and wanted me to be a guest from time to time. I was happy to be on. It’s really cool to talk and do it, but it’s just extremely time consuming. Maybe once I’m no longer working full-time that’s something I can indulge in more often.

I’ll definitely contact J$ about the net worth list. I won’t be anywhere near the top, but it’d be fun to track it along with other bloggers.

Best wishes.

Dividend Pipeline,

Ouch! Man, I’m sorry to hear about that. That’s horrible!

But, at least you can be comforted knowing that the big tax bill was a side effect of receiving so much income. Still sucks to stroke that check, but makes it a little easier. 🙂

I’d definitely look into adjusting your withholding or paying quarterly if this is going to be recurring for you. Otherwise, you’ll definitely be paying fees.

Best of luck next time around.

Take care!

DM,

This was a very timely post for me as well. I’ve been having to pay these huge tax bills annually as a result of the excess dividend income that I earn through the year. It never once occured to me to make estimated payments throughout the year. I’m definitely going to look into setting all of my exemptions to 0. The other complicating factor for 2014 is we now have a larger mortgage and significant interest deductions. I think that should help improve our tax position significantly for 2014. I’d really like to find a good tax tool to run some modelling scenarios to get a view of how much we’d owe.

Integrator,

Hopefully with the new deductions for the 2014 tax year you won’t have a big bill in 2015 whether you pay quarterly estimated taxes or not. Although, setting exemptions to 0 definitely helps with that as well.

I’m single, no children,and I rent, so I don’t have any major deductions at the end of the year.

Best of luck with the new house! 🙂

Cheers.

DM,

I recently sold a large amount of stock which will result in a significant amount of capital gains tax being owed. Can I make a single payment of the estimated taxes due on that sale now through the EFTPS and not be required to pay anything else quarterly until taxes are due next April?

Thanks

Steven Tubbs,

I think this will help:

http://www.irs.gov/Help-&-Resources/Tools-&-FAQs/FAQs-for-Individuals/Frequently-Asked-Tax-Questions-&-Answers/Estimated-Tax/Large-Gains,-Lump-Sum-Distributions,-etc./Large-Gains,-Lump-Sum-Distributions,-etc.

According to the IRS, larger estimated taxes later in the year may be permitted due to large distributions. However, I’m not sure how that affects those that never paid estimated taxes from the beginning.

I hope that helps!

Cheers.

Question: do I actually have to send in any paper documents? Or do I just pay?

David,

There’s no paper documents to worry about. The IRS tracks your payments for you, though I keep a copy of those transactions myself.

When you do file your taxes the following year you then just enter the estimated taxes you’ve already paid which would apply toward any amount you owe.

I hope that helps!

Cheers.